The Fed, FDIC, and OCC clearly adopt a technology-neutral approach to tokenized securities, with capital requirements consistent with traditional securities, removing regulatory concerns in the RWA market.

Federal Reserve Issues Guidance: Tokenized Securities Are Subject to Same Regulatory Capital Standards as Traditional Securities

The U.S. Federal Reserve (Fed), together with the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC), recently released a new FAQ document explaining how tokenized securities are treated for regulatory capital purposes. Regulators explicitly state that banks holding or processing tokenized securities should follow the same capital rules as traditional securities.

The regulatory document notes that the technical form of issuance or trading of securities (such as whether blockchain or distributed ledger technology is used) generally does not alter the capital treatment of the asset. In other words, as long as the legal rights and risk profile of the asset are the same as those of traditional securities, the capital requirements should remain consistent.

Bank regulators indicate that this approach reflects the principle of “technology neutrality.” The legal nature and risk assessment of financial assets are the core factors for capital rules; the issuance format and technological platform do not impact this regulatory standard.

Blockchain Form Does Not Affect Regulatory Requirements; Capital Rules Remain Consistent

In banking regulation, capital adequacy ratio is a key indicator. Banks must hold a certain proportion of high-quality capital and liquid assets as a buffer against market volatility and potential losses.

The regulators explicitly state that if a security is recognized as a qualifying financial asset, its tokenized form does not change how it is accounted for in capital calculations. For example, a tokenized bond or stock on a bank’s books should be treated the same as its non-tokenized version.

Regulators also note that tokenized securities, when compliant with existing legal and risk management standards, can be used as financial collateral. When using these assets as collateral, banks must follow the same haircut and risk management standards as with traditional securities.

Additionally, regulators emphasize that the blockchain type does not influence capital treatment. Whether tokenized securities are issued or traded on permissioned or permissionless blockchains, the regulatory capital rules remain the same.

Rapid Growth of Tokenized Assets Accelerates Clarification of Applicable Regulations

In recent years, financial institutions have actively converted traditional assets such as stocks, bonds, and real estate into digital tokens on blockchain to improve trading efficiency and market liquidity.

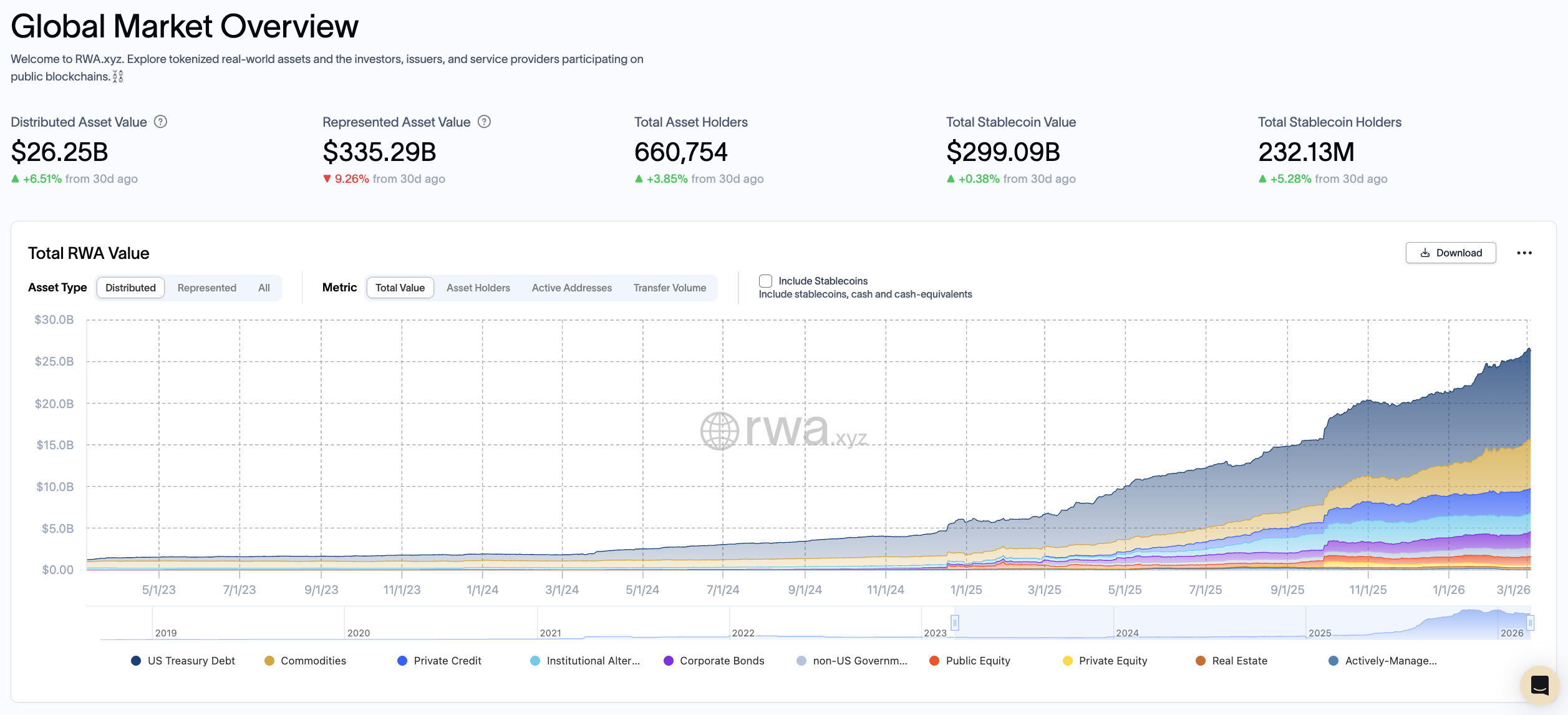

Data from market research firm RWA.xyz shows that the global market size for tokenized real-world assets (RWA) is approximately $26.25 billion, with tokenized U.S. Treasury products accounting for the largest share. The tokenized stock market size is around $110 million, still in early development stages.

Image source: RWA.xyz Global Market Size of Tokenized Real-World Assets (RWA) is approximately $26.25 billion

Industry participants generally believe that tokenized securities can bring multiple efficiency improvements, including 24-hour trading, real-time settlement, and lower transaction costs. Some trading platforms and fintech companies have already launched tokenized stock products in Europe, allowing investors to trade traditional listed company stocks via blockchain.

However, tokenized securities still need to align with existing legal and regulatory frameworks. The U.S. Securities and Exchange Commission (SEC) earlier this year stated that tokenized securities fall under federal securities laws and must comply with registration, disclosure, and investor protection requirements.

Further Reading

Tokenized Securities Are Securities Too! The U.S. SEC Clarifies Regulations and Officially Incorporates Them into Securities Law

Gradually Clarifying Regulatory Attitudes

The recent guidance from the Fed and other banking regulators signals a gradual integration of blockchain finance into the banking system. Over the past few years, U.S. banking regulators have maintained a relatively conservative stance toward crypto assets and blockchain technology, creating high uncertainty for financial institutions pursuing related activities.

As interest in tokenized assets grows among financial institutions, regulators are beginning to clarify how existing financial laws apply to blockchain assets. The core significance of this capital rules clarification is to confirm that tokenized securities will not face additional capital burdens or stricter regulatory treatment solely due to their technological form.

Market analysts note that clarifying capital rules is highly significant for the banking industry. Capital adequacy is one of the core constraints on all banking activities. With clearer regulatory frameworks, banks can better assess the risks and costs associated with tokenized securities.

Tokenized securities are seen as an important bridge connecting traditional finance and blockchain markets. Future collaborations between banks, asset managers, and crypto financial platforms are expected to evolve as regulatory policies continue to develop.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.