For four centuries, from Lloyd’s of London to Wall Street investment banks, the power of “underwriting” has always been held by those who control the place where assets are created. Pump.fun has earned $1.5 billion through token issuance, Raydium’s order flow was drained, causing RAY to crash 70%, and Hyperliquid’s latest HIP-6 proposal attempts to embed a token auction mechanism directly into the consensus layer. This article is based on Prathik Desai’s piece “Underwriting is Software,” edited and translated by Dongqu.

(Background: Bloomberg reports Hyperliquid as the only window to observe oil prices over the weekend, with a spike to $92; now crude oil has surged to $112.)

(Additional context: Oil prices broke $108! Hyperliquid whales shorting crude lost $3.4 million in unrealized gains, with liquidations remaining at $120.)

In 1688, a coffeehouse on Tower Street in London became one of the most important venues in global commerce. Captains, shipowners, and merchants would enter Edward Lloyd’s coffeehouse, holding a note describing cargo, routes, and ships. They needed someone to bear the risks of the voyage. Those willing to take on part of the risk would sign beneath the note. This is the origin of the term “underwriting.”

The most powerful person in the room was the one who decided the terms of the ship tickets, including the premiums charged, the risks assumed, and which voyages to support. Before this person assessed the risk of the maiden voyage, no ship could set sail.

This arrangement helped the coffeehouse evolve over the past three centuries into Lloyd’s of London — one of the world’s largest insurance markets. Interesting, right? When I started reading this story, I uncovered an insight still relevant today: any asset, project, or tradable thing requires a moment when someone decides, “This is worth supporting at this price, under these terms.”

Whenever a new asset class emerges, we see this pattern repeat.

About two centuries after Edward’s coffeehouse, J.P. Morgan supported U.S. railroad projects by issuing stock for companies like the New York Central Railroad. This established Morgan’s reputation as a capital mobilizer and railroad finance expert.

His underwriting set the terms, selected investors, and profited from the spread between the issuance price and the public offering price. If Morgan refused to underwrite a project, it simply wouldn’t be built.

Modern IPOs are digital versions of this mechanism. A few banks underwrite a company’s initial public offering, assess demand, set the issue price, and allocate shares. The stock “soars” on the first day — up 20-30% — which is not just market behavior but reflects the underwriters’ profit margin.

For four centuries, investors’ only complaint has been that insiders received the best allocations, and the initial pricing rarely reflected actual demand, with others entering only after the spread was already taken.

Last week, James Evans posted a HIP-6 proposal for token issuance auctions on Hyperliquid, partly addressing this complaint. On X, he disclosed that he holds $HYPE tokens and collaborates with early crypto venture firm Reciprocal Ventures.

In today’s deep dive, I will evaluate HIP-6 and other on-chain platforms to see if they can address the long-term issues in capital formation.

The traditional book-building process is inherently a black box. Banks solicit demand from institutional clients in closed-door meetings, set prices based on conversations the retail market can never know, and allocate shares to “random” accounts. The issuer gets the issue price, while the public receives the remaining shares.

Consider these two examples:

During Facebook’s (now Meta) 2021 IPO, lead underwriter Morgan Stanley lowered revenue expectations during investor roadshows. This negative info was immediately conveyed to major institutional clients via analyst reports, while retail investors remained unaware. Within three months, Facebook’s stock fell about 50%. Retail investors were further disadvantaged: they paid inflated prices for full allocations but lacked access to insider information.

A more recent example is Rivian’s 2021 IPO. Priced at $78 per share, it soared to $179 on the first day. Institutional clients with allocations from Goldman Sachs and J.P. Morgan captured the spread, while retail investors bought at open. Over ten days, Rivian’s stock dropped about 40%. Investors later sued, alleging Rivian concealed that its vehicle prices were below material costs. The company settled for $250 million but denied wrongdoing. Today, Rivian trades below $16 per share.

This operation has become normalized as a business model, so ordinary investors hardly notice the problem.

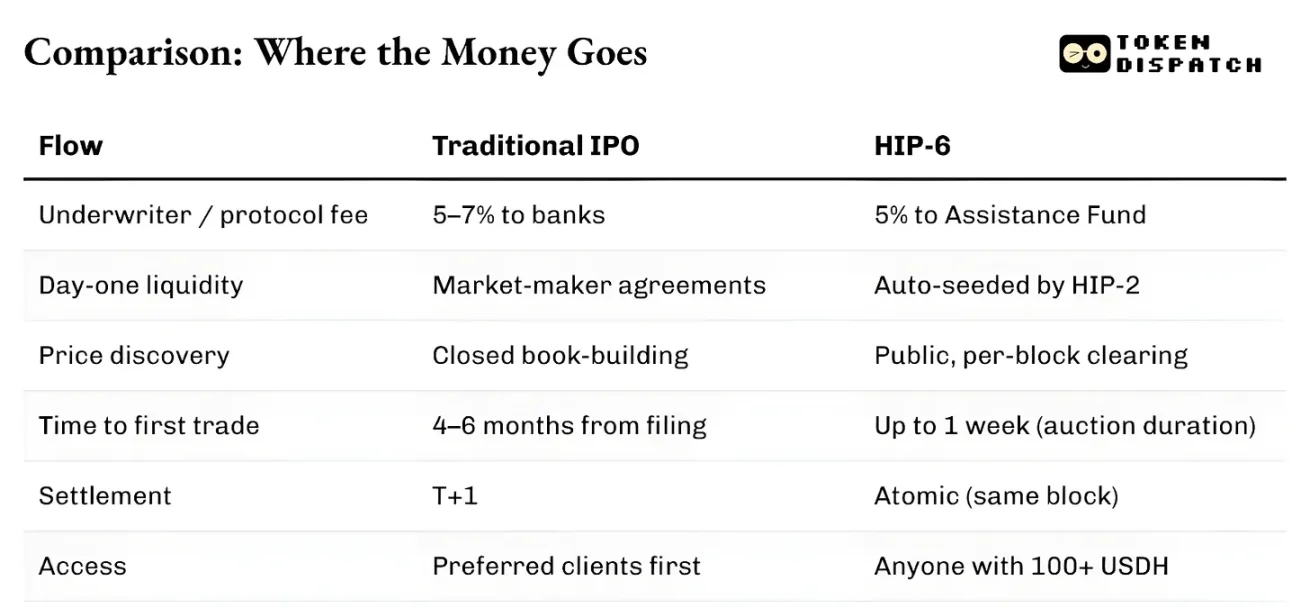

Beyond capital allocation, the entire infrastructure is slow and siloed. From filing to first trade, IPOs typically take four to six months. Settlement requires a full trading day. Assets can’t be used as collateral until settlement completes. Market makers operate under individual agreements, often with spread guarantees. The system is also jurisdiction-dependent. Even if willing to take the same risk, retail investors outside the U.S. can’t participate in NY-based IPOs under equal terms.

The underwriters’ power stems from these frictions. Opaque pricing, settlement delays, and entry barriers are exploited and turned into moats.

On-chain underwriting is structurally different, with less middlemen. Continuous Clearing Auctions (CCA) or binding curves publish all bids in real-time. Liquidity is automated from the first block. It’s encoded into the mechanism itself through calculation rather than negotiation. Assets can be traded and collateralized within the same block memory. No T+1 or settlement cycle delays.

Entry controls still exist but along different lines.

Pump.fun’s issuance is open to all wallets with sufficient funds. Echo’s sales require KYC but can involve participants across jurisdictions. Hyperliquid’s HIP-6 sets a $100 minimum economic threshold but does not restrict participant eligibility. All these systems avoid the “priority client” allocations typical of most traditional book-building.

The key difference is that on-chain underwriting treats each token issuance as a buy order for the ecosystem’s native token (whether SOL, USDC, USDH, or others). Traditional underwriting, aside from the underwriting fee, does not generate ongoing demand.

This difference has a bigger impact than you might think.

On March 20, 2025, pump.fun launched its autonomous AMM, PumpSwap, on Solana. Before this, all tokens graduating from pump.fun’s binding curve were routed automatically to Raydium, Solana’s largest DEX. This token flow became one of Raydium’s main revenue sources. But overnight, this channel was cut.

Raydium’s AMM revenue is estimated to have lost 35-40%. Its token RAY fell 30%. Raydium responded swiftly, launching its own token issuance platform, LaunchLab, within 48 hours. RAY’s price surged, doubling in six months, then plummeted to a two-year low. Since pump.fun introduced its own AMM, RAY has fallen nearly 70%.

The lesson: whoever controls the token issuance location controls downstream fee income. Issuance equals order flow.

The resulting landscape has split into two very different paths.

One is market formation — generating tradable charts at internet speed. Pump.fun exemplifies this, with a binding curve, a $69,000 graduation threshold, and automatic liquidity injection via PumpSwap. It has accumulated nearly $1.5 billion in fees, issued over 16.8 million tokens, and used over 98% of revenue to buy back PUMP tokens, offsetting over 27% of circulating supply.

The other is capital formation — structuring funds for real users under compliant safeguards. Coinbase acquired Echo for $375 million in October 2025, adding a KYC-enabled token sale platform with time-weighted deposit vaults. Echo’s Sonar product contrasts sharply with pump.fun; it employs a regulated, verified, carefully curated approach by lead investors.

Coinbase’s solution’s weakness lies in liquidity at launch. Echo handles distribution but doesn’t automatically activate trading markets.

HIP-6 is the latest attempt to merge these two paths into a single protocol-level primitive.

The proposed mechanism embeds a Continuous Clearing Auction (CCA) into the HyperCore consensus layer. Each block uses a model based on residual block budget differences to calculate the clearing price from all valid bids.

This pattern isn’t new. HIP-6 explicitly adopts Uniswap’s CCA model, launched in November 2025, initially used by Aztec Network, raising $60 million from over 17,000 bidders with no detected sniping or automation manipulation.

Both implementations share the same core idea: splitting large auctions into thousands of smaller, sequential auctions per block, gradually releasing tokens, calculating a unified clearing price each block, allowing bids within a price range to prevent collusion, and automatically injecting liquidity at settlement.

This design addresses the same legacy issues.

Fixed-price sales force investors to guess the opening price. Proportional sales risk a vicious cycle of oversubscription. Dutch auctions enable timed bidding by professionals. CCA eliminates all three. In CCA, the final seed price is a volume-weighted average over the auction window, a measure against manipulation that makes price collusion prohibitively costly.

The difference between Hyperliquid and Uniswap lies in their settlement architecture.

HIP-6 executes directly within HyperCore’s consensus layer. The auction logic runs inside the block transformation function, not as an external contract. Settlement occurs at the same level as trade matching.

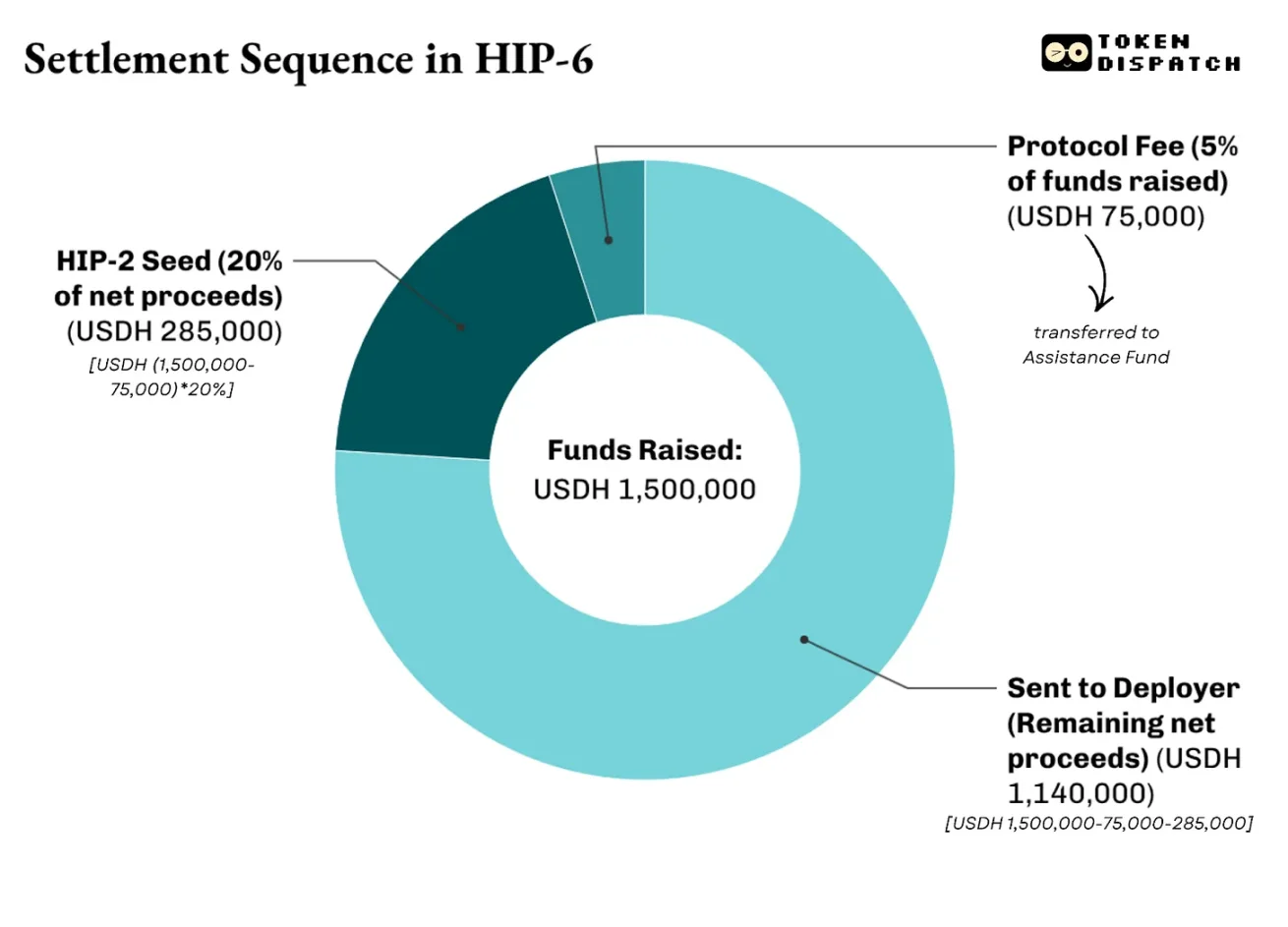

Settlement adopts a multi-tiered structure. The proposal charges a 500 basis point (bps) protocol fee on total funds raised, which goes into an aid fund. Hyperliquid uses this fund to buy back all $HYPE. In net proceeds (after fees), 2,000 to 10,000 bps (20%–100%) are allocated to initiate the HIP-2 market at a derived price. The remaining funds go to the deployer.

For example, a $PROJ token auction on HIP-6 raised $1.5 million USDH, with a total supply of 10 million tokens, 20% of which is seed funding for HIP-2. The settlement is as follows:

This is precisely the difference between HIP-6 and Uniswap.

Uniswap builds CCA as a token issuance tool to fund its existing AMM pools. With HIP-6, Hyperliquid becomes a full-stack infrastructure enabling stakeholders to raise capital, discover prices, build bilateral liquidity, and start trading on a centralized limit order book (CLOB).

More importantly, all of this is denominated in the asset the protocol expects you to hold — $1000 USDH.

While transparent price discovery, programmatic liquidity, and atomic settlement are significant improvements over traditional models, on-chain underwriting also introduces a series of inherent issues.

These mechanisms can’t solve project quality problems. Pump.fun’s binding curve ensures price fairness but doesn’t reflect the credibility of the project behind the token. HIP-6 openly admits this flaw. It doesn’t address token quality, governance, or holder protections.

Traditional underwriters bear reputation and legal liabilities if issuance fails. Listing a bank’s name on a prospectus indicates stakeholder review of the issuer. On-chain mechanisms can’t provide similar accountability pathways. Coinbase’s Echo approaches this with KYC, issuer disclosures, and sales restrictions, but reintroduces entry barriers that on-chain underwriting aims to eliminate.

In most major jurisdictions, whether a token issuance constitutes a security offering remains unresolved. The easing of U.S. enforcement makes permissionless token issuance easier, but legal uncertainties persist.

However, since we are still in early stages, I expect future improvements to make on-chain underwriting a better alternative to traditional capital formation systems.

In finance, the entity controlling the asset’s place of origin always earns the most enduring fees.

From 2012 to 2021, Goldman Sachs led U.S. IPOs more than any other bank. But the benefits go far beyond the hefty fees. Once Goldman underwrites a company’s IPO, it often becomes the main advisor for subsequent offerings, mergers, and debt issuances.

We see that pump.fun, by providing a reliable platform that generated over $1 billion in revenue from 16.8 million tokens, exemplifies this. Raydium’s crash follows a similar pattern: once it lost control over the token issuance process, its 35-40% revenue vanished overnight.

With on-chain underwriting, the system remains the same; only the entity changes. It’s no longer a bank or underwriter but a protocol. This protocol offers a transparent, auditable token distribution process without relying on insiders.

In return, it expects you to use a unit of account — its native token — for all transactions. I see this as a beneficial trade-off for investors. Stable demand for the native token leads to locked-in circulating funds, boosting liquidity.

This makes competition fierce not only between traditional and on-chain underwriting but also among on-chain participants. The contest has shifted from secondary market battles to control over initial pricing, token allocation, and which currency investors must use.