Author: Frank, PANews

On March 8, Pump.fun’s total revenue surpassed $1 billion, making it the first platform on Solana to reach this milestone and firmly establishing itself as the most prominent money printer in the MEME sector. But after the hype subsided, the question is no longer just “who makes the most money,” but rather how much business these MEME-originated platforms still have left.

Looking at leading projects like Pump.fun, GMGN, Four.meme, Axiom, as well as Photon, BullX, and BONK, the answer is becoming clearer: MEME hasn’t disappeared; instead, business is increasingly concentrated among the top players, with differentiation between chains and platforms becoming more pronounced.

Pump.fun: The “Absolute Oligarch” Crossing Bull and Bear, Earning Hundreds of Millions Yet Hard to Consolidate

If the previous MEME craze was a nonstop gold rush, then Pump.fun was undoubtedly the most profitable toll booth in this gold town. Public data shows that by March 2026, Pump.fun’s total accumulated revenue exceeded $1 billion. Of this, about $321 million was generated in 2024, expanding to approximately $664 million in 2025. Starting in 2026, the MEME industry experienced a severe downturn, but Pump.fun’s influence seemed relatively unaffected, still earning about $98.3 million to date.

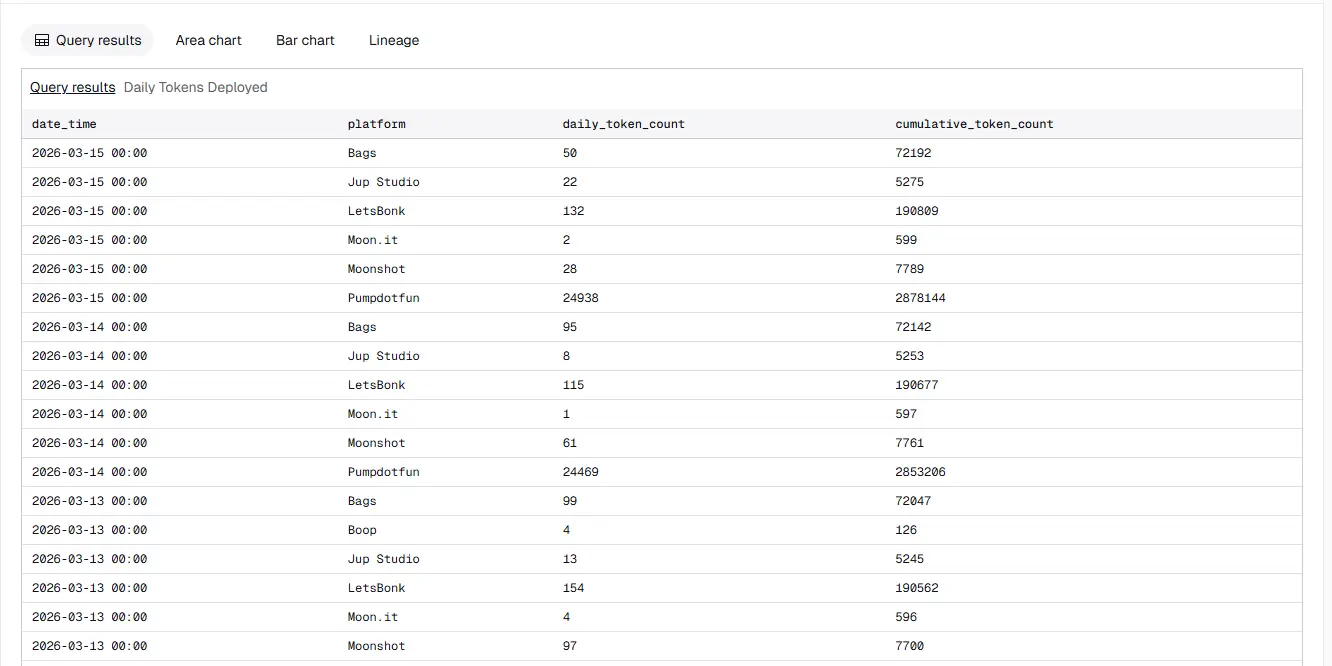

Market-wise, Pump.fun’s dominance within the Solana ecosystem has further strengthened. For example, on March 15, Pump.fun’s token creation accounted for 99.1%, with graduation tokens at 94.8%, and daily trading volume making up about 93%. On that day, Pump.fun issued 24,938 tokens, while LetsBonk only 132, Bags 50, Moonshot 28—other token launches are no longer competitive with Pump.fun in daily volume.

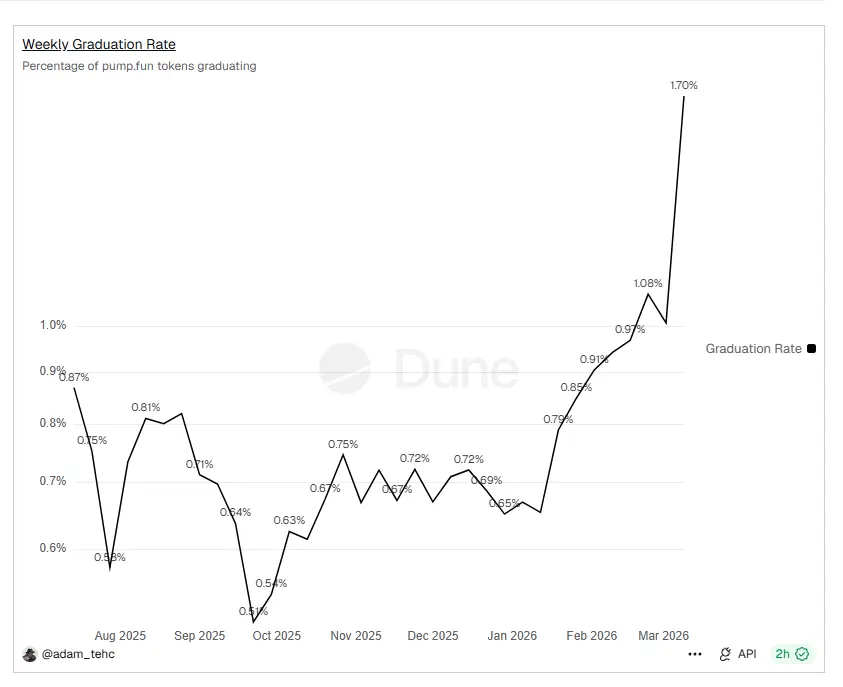

Looking back at Pump.fun’s own data, it maintains a surprisingly high level. Over the past two weeks, rough estimates show an average of about 29,700 tokens issued daily, around 157,700 active wallets daily, with daily trading volume roughly $93.65 million, and daily revenue about $870,000. Meanwhile, the long-criticized graduation rate has shown signs of recovery, even reaching around 1.70%. Although this short-term spike’s exact cause is unclear, Pump.fun’s graduation efficiency is indeed improving.

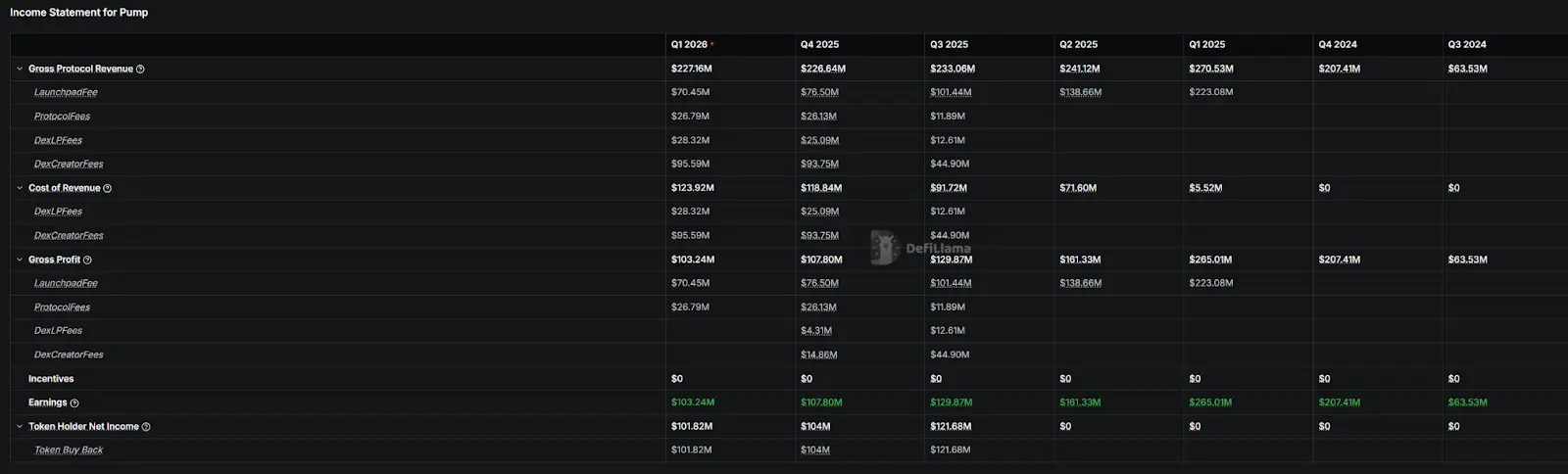

However, while fee generation remains steady, this doesn’t mean all income fully translates into protocol profits. First, more than half of the fees are shared with creators and LPs. Second, aside from creator earnings, remaining revenue is used for token buybacks. In Q1 2026, Pump.fun generated about $227 million in fees, with $123 million paid to creators and LPs, and nearly all of the remaining $100 million used for buybacks.

But the problem is, buybacks haven’t automatically driven up the token price. As of March 16, PUMP was about $0.002, still 76.21% below its all-time high of $0.0088. A more reasonable explanation is that buybacks mainly serve as a floor and narrative support, but are insufficient to reverse the valuation compression trend across the MEME sector. In other words, Pump.fun’s cash flow engine is still running at high speed, but the market is no longer willing to assign it higher multiples just because “it makes money,” as in the previous hype.

In summary, Pump.fun’s market landscape remains relatively stable. Although the entire meme coin sector is declining, most competitors are dying out, which only strengthens Pump.fun’s dominance. If another wave of MEME hype occurs, it will likely benefit Pump.fun the most.

GMGN: Quarterly Revenue Grows Fivefold, BSC Becomes the “New Traffic King”

GMGN’s revenue saw another explosive growth in Q1 2026. Total revenue for the first quarter reached $25.31 million, nearly five times the $5.64 million in Q4 2025. This quarter’s revenue is also the second-highest in GMGN’s history (only behind $40.81 million in Q1 2025).

Breaking down this revenue structure, the main driver is BSC. Starting October 2025, GMGN’s trading volume on BSC significantly surpassed Solana, and by 2026, this trend stabilized. Currently, BSC trading volume on GMGN accounts for nearly three times that of Solana.

Overall, user activity and trading volume in GMGN increased in Q1 2026, but the growth wasn’t as dramatic as the revenue figures suggest. This indicates that the revenue spike in Q1 was real but possibly inflated by DefiLlama’s data issues (BSC revenue data was empty before October 2025). The surge mainly resulted from a spike in MEME trading volume on BSC in January, with total chain revenue reaching $16.34 million that month, dropping to $5.18 million in February, and about $3.77 million so far in March. The first quarter’s overall level is close to the same period in 2025.

Four.meme: The “Face” of BSC, Daily Income Only a Fraction of Peak

If Pump.fun has absorbed most of Solana’s launch platform traffic, then Four.meme is the closest equivalent on BSC.

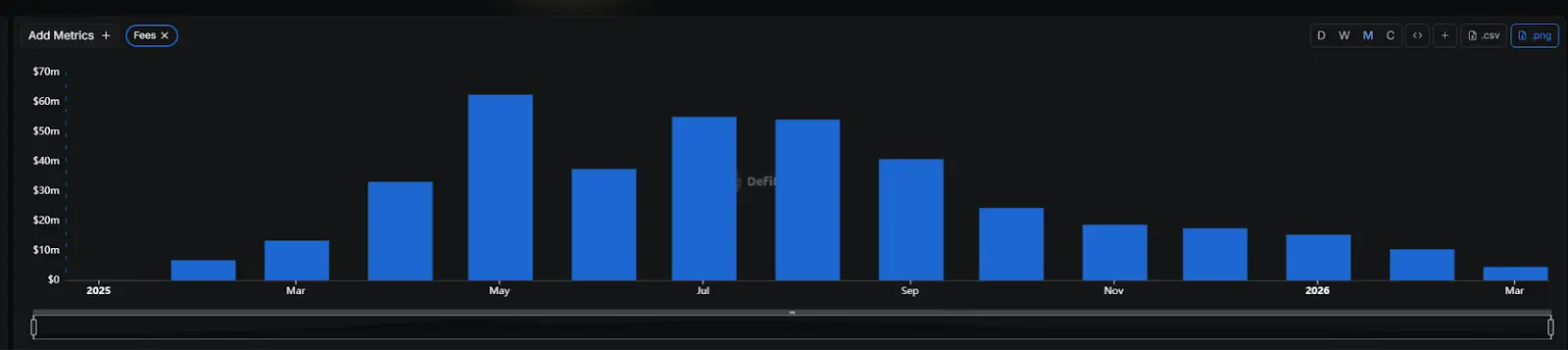

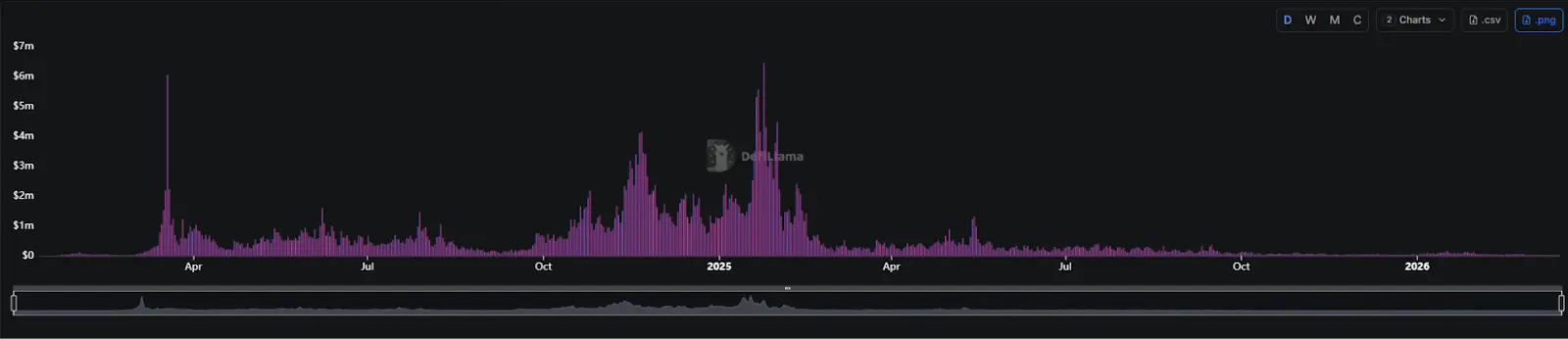

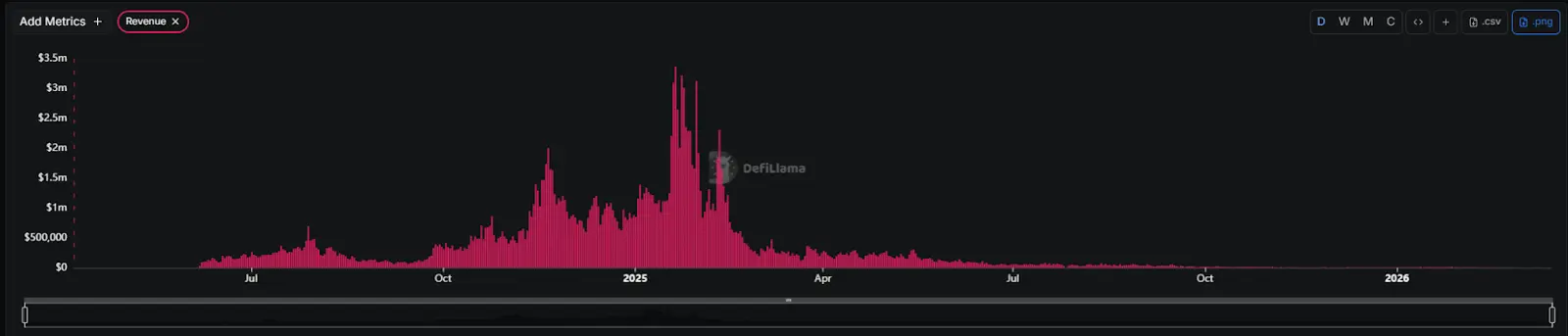

DeFiLlama data shows that as of March 16, Four.meme’s Q1 2026 protocol revenue reached $16 million, significantly lower than $54.24 million in Q4 2025, but monthly revenue has shown slight recovery.

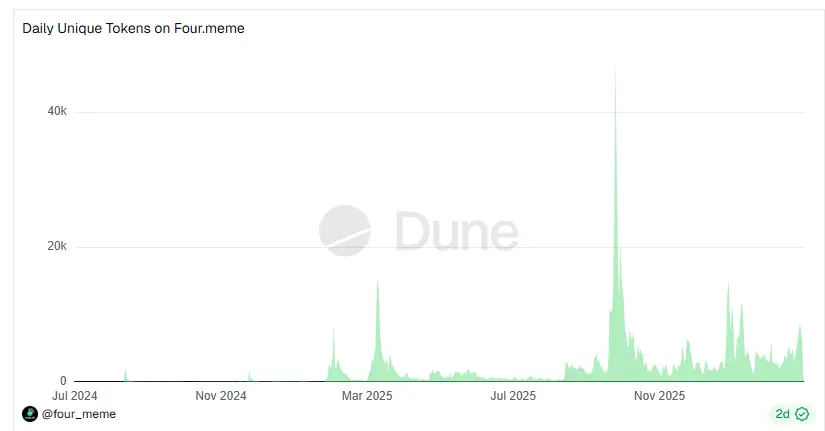

Recent 10-day data tracked by Dune shows Four.meme issues about 4,858 tokens daily, with roughly 5,749 active users daily, but only about 25.7 tokens are actually listed on PancakeSwap, with a further drop in short-term graduation rate to around 0.53%. Compared to the peak daily average revenue of $4.22 million in October 2025, current income has fallen to $20–30K.

In contrast, Pump.fun’s recent two-week data shows an average of about 29,700 tokens issued daily and roughly $93.65 million in daily trading volume. Clearly, as the main MEME platforms on Solana and BSC, Four.meme and Pump.fun differ greatly in scale and token quality, reflecting the development status of MEME on these chains.

Axiom: Moving Away from High Growth, Falling Into a Volume Drought

If GMGN’s growth in Q1 2026 was mainly due to BSC’s rotation, Axiom’s situation is almost the opposite.

DeFiLlama data shows that Axiom’s revenue in Q1 2026 is about $29.03 million, higher than GMGN’s $25.31 million.

However, Axiom faces a continuous decline. According to quarterly revenue data, Axiom’s protocol income peaked at $133 million in Q2 2025 and $150 million in Q3 2025, then fell to $60.66 million in Q4 2025, and so far $29.03 million in Q1 2026. Compared to its most frenetic phase last year, its scale has shrunk significantly. Unlike GMGN, which still occasionally rebounds, Axiom seems unable to recover.

For Axiom, it is no longer just a tool riding the MEME hype but has become a mature trading machine tested through multiple cycles. Compared to GMGN, which still has growth potential, Axiom’s future seems to be shrinking.

Photon, BullX, and BONK: “Fallen Behind” After the Tide Recedes

Compared to the rebounding GMGN and the still-strong Axiom, Photon, BullX, and BONKbot’s revenue curves in 2026 show more obvious downward trends.

DeFiLlama data as of March 16 shows Photon’s total revenue around $438 million, but quarterly income has declined sharply from $122.8 million in Q1 2025 to $32.31 million in Q2, $18.99 million in Q3, $5.29 million in Q4, and only $4.52 million so far in Q1 2026, showing a near-step decline.

BullX’s total revenue is about $203 million, with quarterly income dropping from $87.37 million in Q1 2025 to $14.25 million in Q2, $3.86 million in Q3, $0.878 million in Q4, and just $49,100 in Q1 2026.

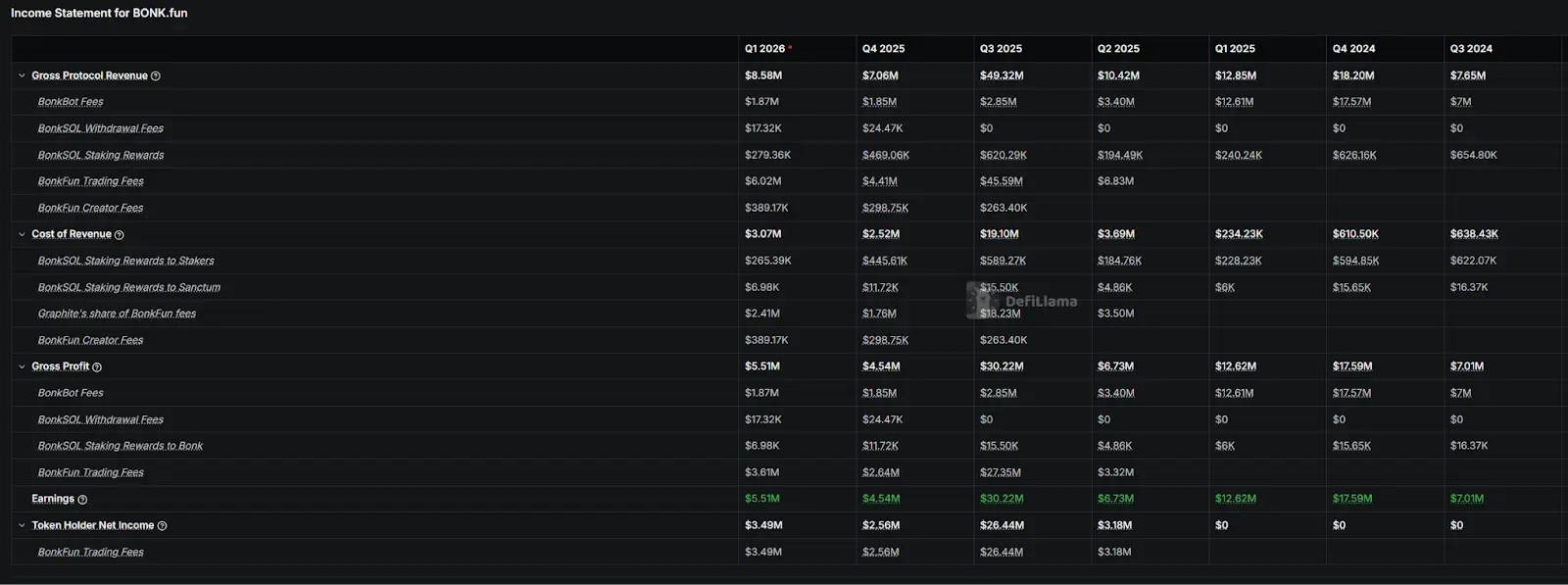

BONKbot’s decline is less steep but still evident. Its total revenue is about $93.57 million, with Q1 2025 at $12.61 million, then falling to $3.4 million in Q2, $2.85 million in Q3, $1.85 million in Q4, and $1.84 million so far in Q1 2026.

However, the BONK ecosystem itself hasn’t completely faded. As of now, BONK.fun’s protocol revenue in Q1 2026 is about $8.51 million, higher than $7.06 million in Q4 2025. The current quarter includes roughly $6 million from Bonk.Fun and about $1.84 million from BonkBot.

Looking at this MEME coin “escape,” one conclusion is clear: the MEME sector hasn’t vanished; the era of wild competition has ended, and the reshuffle is happening much faster than expected.

After the tide recedes, the platforms that remain are no longer just the fastest runners but those that have built a complete closed-loop system of launch, trading, liquidity, and fee collection. If the next MEME cycle ignites again, these are most likely to be the first to reap the benefits.