Author: Chen Mingkun Macro Observation

This article mainly answers five questions:

First, when war arrives, what does the market re-evaluate first;

Second, why do different wars correspond to different asset narratives;

Third, which four dynamic war mechanisms rewrite which layers of variables;

Fourth, which modern war asset samples are most worth revisiting repeatedly;

Fifth, how to implement war judgments into methodology and positioning.

If you’re more concerned about investment positions, you can go directly to Part Five.

Many people see war first through the news.

But macro investors often don’t focus on the news itself, but on: asset rankings beginning to change.

In the past month, as conflicts reignited in the Middle East, I repeatedly reviewed historical conflicts and asset evolutions in modern warfare at my desk in Tsinghua Purple Bamboo Park, increasingly confirming one thing:

The first thing war changes is often not the world order, but asset rankings.

In my view, the most important aspect of studying war and assets is not stance, emotion, or trying to claim interpretive authority. The real key is:

Break down war into variables, anchor those variables to prices, and then translate prices into positions.

Therefore, a more important question than “What to buy when war comes” is:

When war arrives, what does the market re-evaluate first?

This article is written for serious traders. It’s not for spectators, nor for those hoping to hear “What to buy in war.”

If next time a major shock hits and you can be less swayed by herd mentality, more judgmental; less emotional, more methodical—then this article is worth reading.

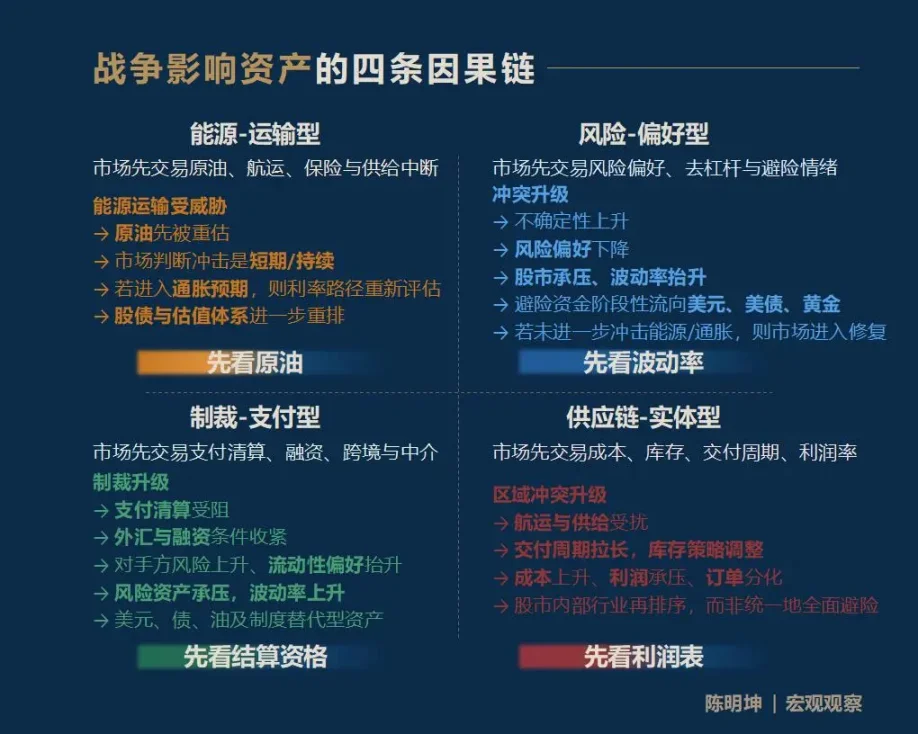

1. War impacts assets not with a single answer, but through four pathways

To start with the conclusion: war influences assets not with one unified answer, but through four completely different transmission channels:

- First, energy-transportation type war.

The market first trades oil, shipping, insurance, and supply disruption risks.

- Second, risk-preference type conflict.

The market first trades volatility, risk appetite, deleveraging, and safe-haven sentiment.

- Third, sanctions-payment type war.

The market first trades payment, clearing, financing, cross-border settlement, and financial intermediary functions.

- Fourth, supply chain-physical conflict.

The market first trades costs, inventories, delivery cycles, profit margins, and industry reordering.

For investors, the most important thing isn’t knowing all answers, but quickly identifying the variable that is re-evaluated first amid market noise.

I call it: the first-priority variable.

Whoever captures the first-priority variable will more easily understand subsequent price paths.

Rash conclusions about assets during conflict are often the easiest to be corrected by the market.

If we compress this framework into a memorable phrase, it’s:

- Energy-transportation: watch oil first;

- Risk-preference: watch volatility first;

- Sanctions-payment: watch settlement eligibility first;

- Supply chain-physical: watch profit statements first.

It’s important to clarify that these four causal chains are not exhaustive, but entry points.

War’s impact on assets often propagates along longer, more detailed, and more complex chains. For example, how does the current Israel-Iran conflict affect grain prices six months later? Natural gas impacts fertilizers, fertilizers impact food, and food impacts inflation and assets of vulnerable countries—such paths are equally valid.

What I aim to offer is not fixed answers, but a macro observation method: enabling each market participant to build their own causal chains based on this perspective.

When war comes, which variable will first become the market’s primary language?

2. Four common misconceptions that are easily misjudged during war

Before diving into specific analysis, I want to clarify the underlying mindset:

“Falsifiability.”

I don’t believe in vague notions of “correctness” that can’t be grounded in prices and positions.

The true value of war research lies in placing judgments into the market and subjecting them to testing.

Meaningful research conclusions are those that can be falsified.

Past facts are used to confirm or falsify previous judgments; future profits or losses are used to confirm or falsify current judgments (harsh but true).

When conflicts escalate, the most common market phrases almost immediately appear:

“Gold will definitely rise.”

“Bitcoin is digital gold, safe haven.”

“Oil prices rise, stocks must fall.”

“Defense industry benefits, buy defense stocks.”

The problem with these statements isn’t that they are necessarily wrong,

but that they are too quick, too neat, too much like common sense.

This kind of thinking is fundamentally “carving a boat to seek a sword”—war doesn’t produce a single-directional effect, but a series of pricing processes with different rhythms, levels, and causal logics.

Therefore, before analyzing the dynamics of war assets, it’s essential to clear away these most easily misjudged intuitions.

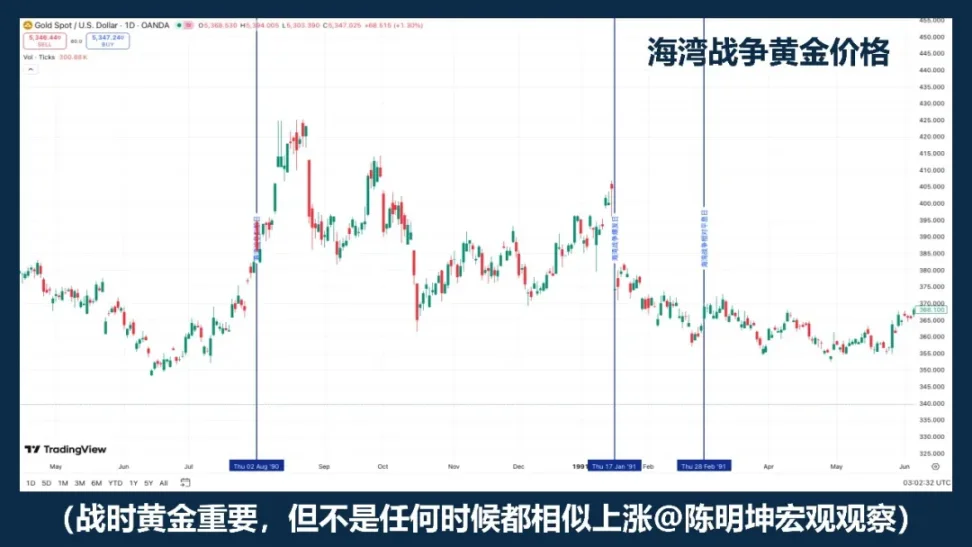

01 | Is it correct to buy gold during war?

Gold is certainly one of the assets most worth observing during war.

If “war = gold rises” were a reliable formula, then gold in different war samples should at least generally move in the same direction.

But historical prices tell a different story.

Catchphrases often hinder thinking.

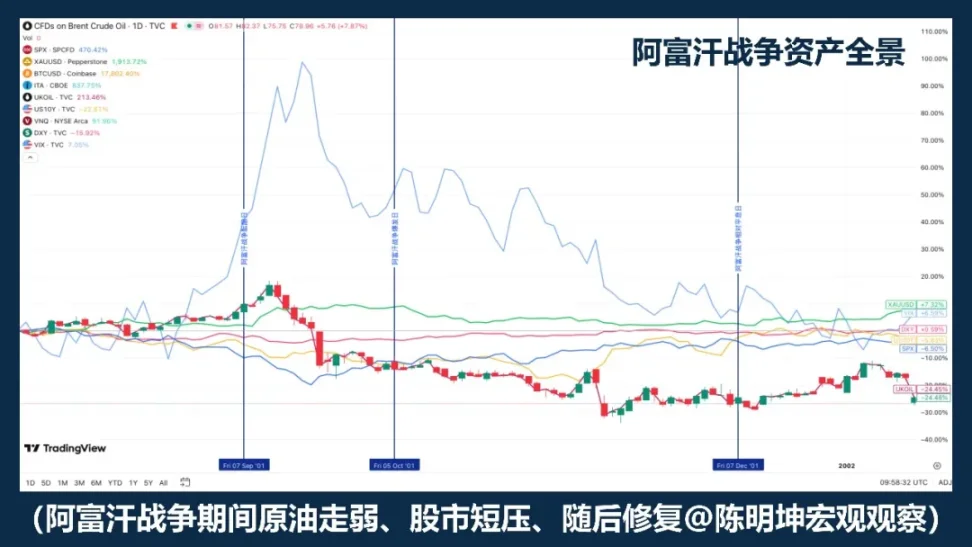

The 1999 Kosovo War is a good example. Intense conflict itself does not automatically lead to a unilateral rise in gold.

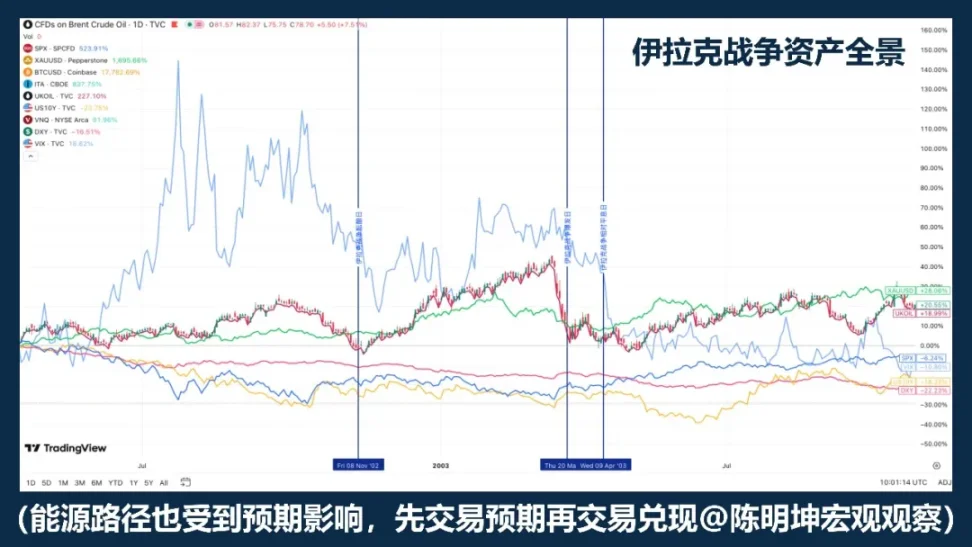

The 2003 Iraq War reveals another structure: gold tends to be bought in the early stages of rising war expectations, then falls back and oscillates after the war officially begins.

Rigobon and Sack’s research on Iraq war risk also supports this: when war risk rises, oil prices, stock prices, US Treasury yields, credit spreads, and the dollar all respond significantly, but gold does not show the same robust statistical response.

What’s truly worth remembering isn’t a specific year, but a more important fact:

Gold often trades not the war itself, but the war expectation.

A more precise way to say it isn’t “buy gold during war,” but:

Gold is usually a priority asset to observe during war, but not a mechanical long position trigger.

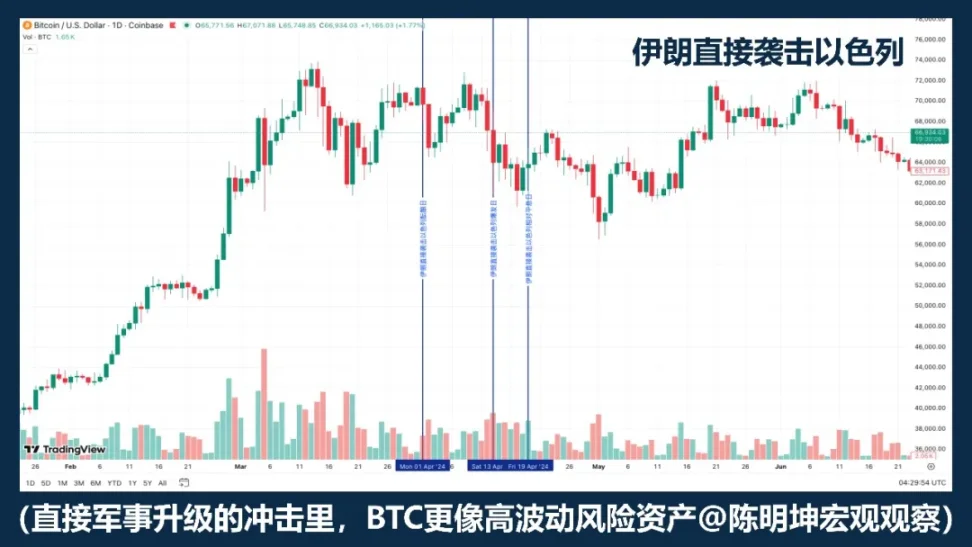

02 | Is Bitcoin a safe-haven asset?

Simply classifying BTC as “a safe-haven asset” is itself imprecise.

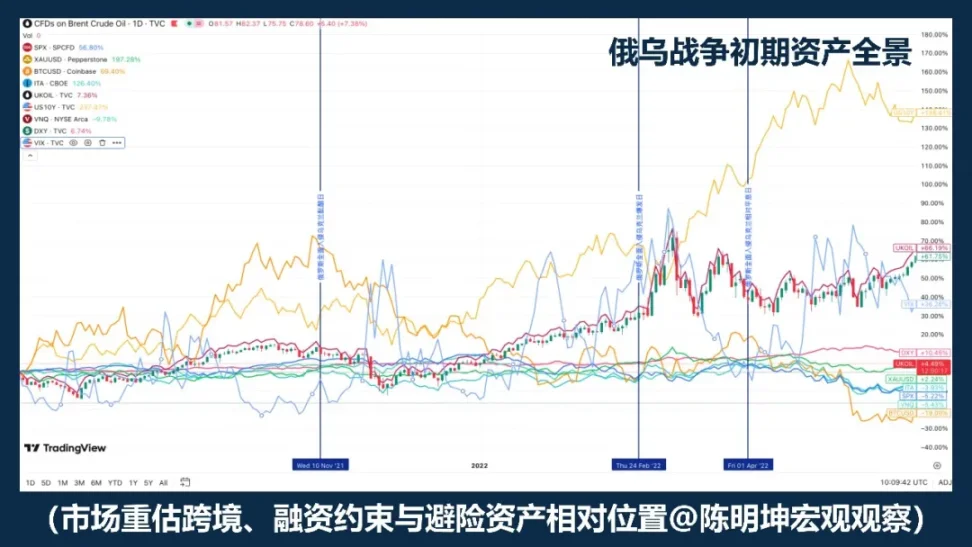

If every war caused BTC to rise, then its performance across different war samples should be relatively consistent. But from Russia-Ukraine, Israel-Hamas, to recent Middle East escalations, the facts show it sometimes falls, sometimes rises, sometimes first drops then stabilizes.

This alone indicates:

War is not the direct causal variable for BTC’s rise or fall.

If the market’s first response is liquidity contraction, risk aversion, and deleveraging, BTC tends to behave more like a high-volatility risk asset rather than a safe haven. Because in such scenarios, the assets first sold are usually high-volatility, high-beta, quickly liquidatable assets.

In other words, often war doesn’t prompt the market to “buy it as a hedge,” but to reduce all high-volatility assets simultaneously.

In this context, BTC behaves more like a risk-oriented tech asset than a safe haven.

But that doesn’t mean it lacks uniqueness.

Its biggest difference from gold is that it’s not only a tradable asset but also a digital asset that can be transferred across borders, operates 24/7, and doesn’t rely on a single banking system.

So, a more accurate statement isn’t “Will BTC hedge during war,” but:

BTC is not a mechanical safe-haven asset during war.

It will be alternately treated by the market as a risk asset, liquidity asset, or alternative settlement tool at different stages.

War doesn’t directly determine its rise or fall.

What truly influences it is which attribute the market prefers to trade at any given moment.

03 | If oil rises, do stocks necessarily fall?

This is one of the easiest statements to accept in war research.

Middle East conflicts often lead to oil prices moving first, which is correct. Because the conflict involves not just ordinary risk but energy transportation itself. EIA data is straightforward: in 2024, about 20 million barrels/day of oil pass through the Strait of Hormuz, roughly 20% of global liquid oil consumption; about 20% of LNG trade also passes here. Once the market worries about this route, oil prices tend to be the first to be repriced.

But the problem is, rising oil prices don’t necessarily mean stocks fall.

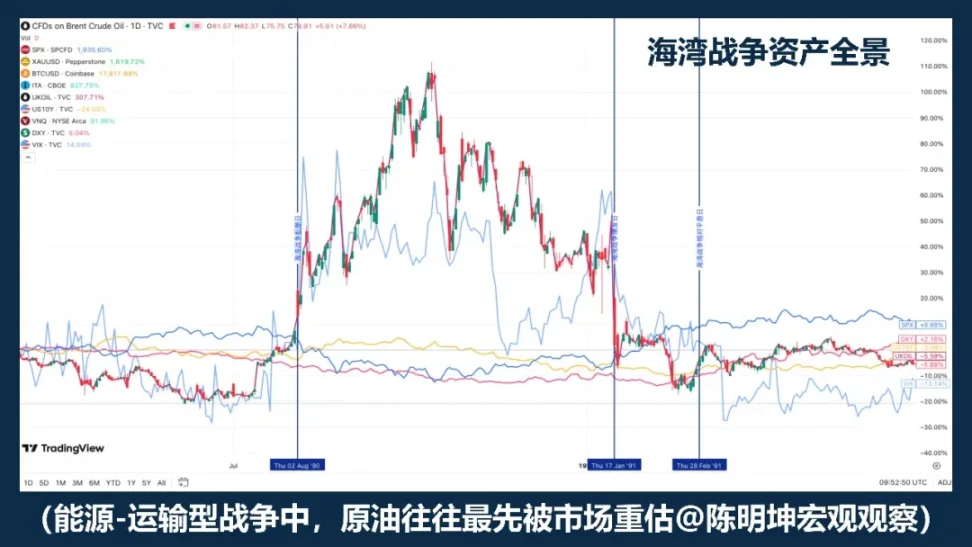

The Gulf War’s history teaches us that “oil up, stocks down” can be the initial response; but as the war situation clarifies and the worst-case scenario doesn’t continue to escalate, markets tend to recover and stocks rebound.

Libyan conflicts provide another example: a closer look shows “oil up, stocks down” is not the true logic of war.

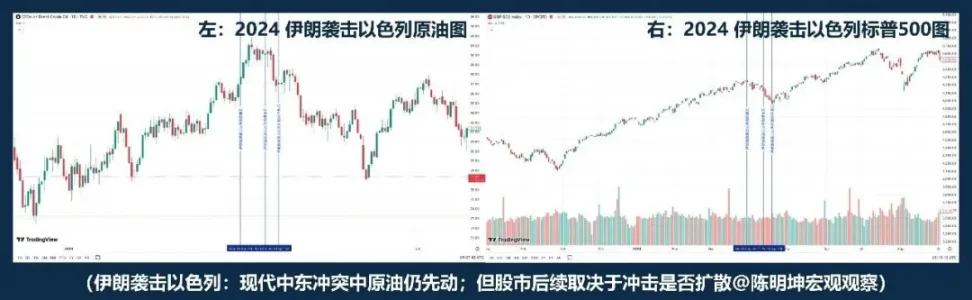

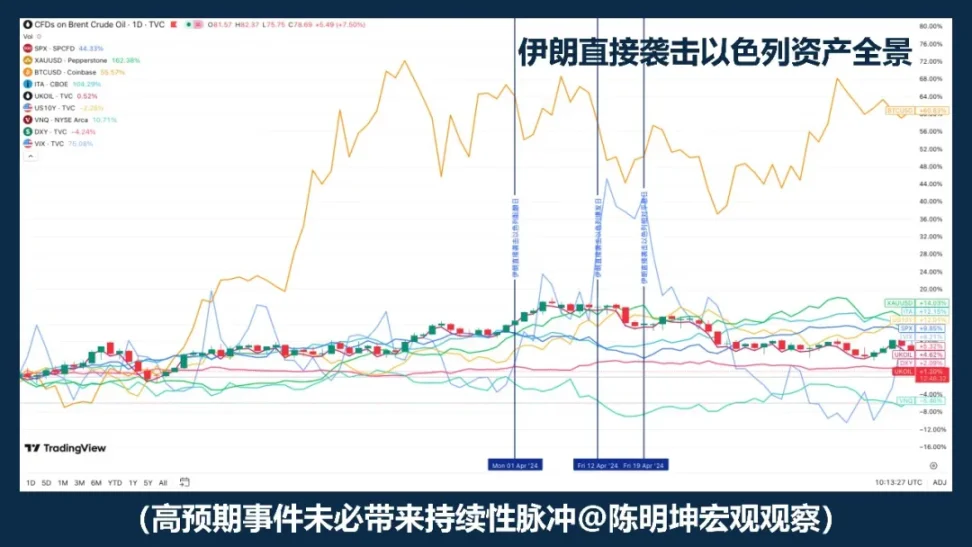

If the Gulf War and Libyan war are relatively distant, the 2024 Iran attack on Israel offers a more recent example. Oil initially surges, then between outbreak and resolution, “oil down, stocks down”; but the S&P 500 did not enter a systemic decline because of it.

Rigobon and Sack’s research on Iraq also found that when war risk rises, it’s not just oil that moves, but oil prices, stocks, US Treasury yields, credit spreads, and the dollar all move together. In other words, the market isn’t just trading oil, but simultaneously trading growth, inflation, safe assets, and financing conditions.

So, the real key isn’t “oil up or not,” but three follow-up questions:

First, is this energy shock short-term or long-term?

Second, will it lead to medium-term inflation expectations?

Third, will central banks revise their interest rate paths?

Therefore, a more accurate statement isn’t “oil up, stocks down,” but:

Oil prices rising are often the starting point of war pricing; how stocks move afterward depends on whether this shock further rewrites growth, inflation, and interest rate expectations.

04 | War benefits, do defense stocks necessarily profit?

The phrase “war benefits defense” is not wrong, but it’s too easy to make people think they’ve understood.

Logically, it makes sense:

When tensions rise, security concerns increase, defense budgets are revised upward, order expectations expand, and defense stocks seem naturally benefitting.

But the market isn’t that simple.

Industry benefits don’t mean stock prices will immediately rise;

rising stock prices don’t necessarily beat the market.

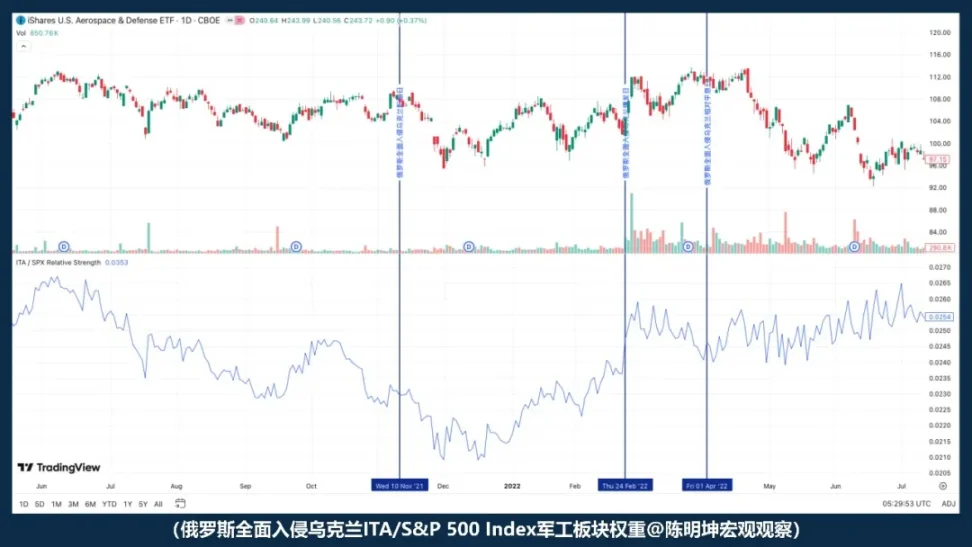

After the full-scale invasion of Russia-Ukraine, the relative strength of the ITA index versus the S&P 500 didn’t strengthen but weakened. That is, at the moment war breaks out, the market doesn’t immediately trade on “defense industry benefits.” Instead, it first reacts to broader forces: risk appetite, liquidity, macro uncertainty.

So, a more accurate statement isn’t “war benefits defense, buy defense stocks,” but:

War raises the narrative around defense, but at the moment of outbreak, what the market prices first isn’t orders, but risk appetite.

Whether defense stocks outperform depends not only on the logic being correct,

but also on valuation, expectation gaps, and which layer of variables the market trades first.

The most dangerous thing during war isn’t lack of opinions,

but having opinions too quickly.

3. The real question: When war arrives, what does the market re-evaluate first?

After dissecting these misconceptions, the core question emerges:

War isn’t a single variable directly determining asset prices; it’s more like a trigger.

What truly influences market reactions isn’t just the conflict itself,

but the war type, macro cycle, expectation gaps, and most critically, the first-priority variable.

So, the question isn’t “What benefits or harms from war,” but:

Which language will the market use first to price it?

Next, the focus shifts from emotional judgment to four real war-driven asset pricing dynamics.

4. Four war dynamics: understanding war starts with identifying its type

Understanding war isn’t just about the battlefield.

More importantly, it’s about judging: which layer of variables it first rewrites.

01 | Energy-transportation war

“Why is oil always the first to be captured by the market?”

The easiest to trigger immediate “pricing” is energy-transportation war.

Common features of this type of conflict aren’t about intensity, but about hitting the upper stream of the global economy:

Oil-producing regions, straits, tankers, ports, shipping insurance, energy routes.

Once these points are threatened, the market’s first re-evaluation isn’t stocks, gold, or macro growth itself, but closer to physical supply-side variables:

Oil and transportation risks.

Oil’s frequent early movement isn’t because it’s “naturally sensitive,” but because of its unique position in the modern economy: both a basic industrial input and an upstream inflation variable.

As soon as the market doubts transportation disruptions, insurance hikes, rerouted routes, or supply contraction, oil is the first to be priced.

In energy-transportation wars, oil isn’t just a reactive asset but the most direct risk carrier.

But a crucial detail is:

Oil often moves first, but doesn’t necessarily keep rising.

The Gulf War is a classic example. During the pre-war period, oil already surged; after the outbreak, prices continued upward; but as the war situation clarified, prices quickly fell back.

The Iraq War further reveals a layered structure: during the expectation-building phase, oil and gold had already reacted in advance; when the war officially started, markets tended to “buy the expectation, sell the fact.” This means that in energy-transportation wars, while oil is usually the first-priority variable, its price path heavily depends on two things: whether it was already fully priced in beforehand, and whether the worst-case scenario materializes after the event.

Therefore, understanding this type of war isn’t just about “oil prices up or down,” but about two layers of context:

First layer: expectation gap. If the event exceeds expectations, oil pulses more sharply; if it’s already heavily discussed and priced in, even a formal conflict can lead to quick oscillation or a sell-the-fact.

Iran’s direct attack on Israel is a typical example: the risk wasn’t unanticipated, so assets pulse but don’t necessarily extend into a sustained revaluation.

Second layer: macro cycle. If it occurs in a low-inflation, policy-space-ample environment, markets tend to see it as a temporary disturbance;

If it happens in a high-inflation, tight-monetary environment, markets immediately ask: will this push oil into medium-term inflation expectations? Will it delay policy shifts?

This is the key difference between energy-transportation wars and other types. Its impact starts from the physical world, propagates along this chain:

Energy transportation threatened

→ Oil is revalued first

→ Market judges whether impact is short-term or persistent

→ If inflation expectations are involved, interest rate paths are re-evaluated

→ Stock and bond valuations are further reordered

The most important takeaway isn’t “oil must rise,” but that:

Oil is often the first upstream variable to be traded by the market.

But oil’s initial move doesn’t automatically mean a long-term trend.

What truly determines the subsequent path isn’t the oil price itself,

but whether oil prices continue to feed into inflation expectations, discount rates, and valuation systems.

In this logic, oil’s first move isn’t the conclusion but the starting point of financial transmission.

02 | Risk-preference war

“The first thing the market revalues isn’t oil, but risk appetite.”

This type of war primarily rewrites the market’s risk tolerance, not physical constraints.

If the conflict doesn’t directly threaten oil-producing regions, straits, tankers, or critical energy infrastructure, then the market’s first re-evaluation isn’t supply constraints, but risk appetite itself.

The initial driver isn’t “energy will be cut,” but “uncertainty will spike, and risk assets dare not hold.”

The first transmission chain usually is:

Conflict escalation

→ Uncertainty rises

→ Risk appetite declines

→ Stocks under pressure, volatility rises

→ Safe-haven funds flow into dollars and gold

→ If no further energy or inflation shocks, markets then recover

This causal chain explains an important phenomenon:

Why after some conflicts, stocks initially fall and gold reacts, but prices don’t automatically trend into a long-term trend. Because this type of war first hits the willingness to hold positions, not deeper supply, inflation, or discount rate variables.

IMF’s research on geopolitical risks also shows that major military conflicts, through rising risk aversion, tightening financial conditions, and spreading uncertainty, significantly impact stock and options pricing. In other words, at this stage, the market is trading not a physical shortage but a re-pricing of volatility and tail risks. The initial decline reflects risk discounting, not a long-term valuation shift. Only if risk appetite continues to decline and propagates into deeper macro variables does this emotional pulse evolve into a lasting asset reallocation.

Thus, a more accurate conclusion isn’t “gold must rise during war,” nor “stocks must fall,” but:

In this logic, the market’s first re-evaluation is usually of volatility and risk assets; the initial decline is more risk discounting than a long-term trend.

03 | Sanctions-payment war

“Payment-type war first rewrites not prices, but qualification.”

The core of sanctions-payment war isn’t about a single commodity’s price, but about cross-border financial system accessibility.

When conflicts escalate to sanctions, the market’s first re-evaluation often isn’t supply, but: payment, settlement, reserves, financing, and counterparty credit.

The Russia-Ukraine war is a typical example. Post-2022, the EU imposed financial sanctions on Russia, including restricting access to EU capital and financial markets, banning transactions with the Russian Central Bank, removing several Russian banks from SWIFT, and freezing or restricting certain Russian assets. The US Treasury’s OFAC also prohibited US persons from engaging in related transactions with Russia’s central bank, sovereign wealth fund, and finance ministry. At this stage, the market faces not just “will oil be cut,” but a deeper issue: can the existing cross-border financial chain still operate normally?

The typical transmission isn’t a direct price move, but a progression from qualification to price:

Sanctions escalate

→ Payment and settlement are blocked

→ Foreign exchange and financing conditions tighten

→ Counterparty risk and risk appetite rise

→ Risk assets under pressure, volatility increases

→ USD, US bonds, oil, and some alternative settlement assets are repriced

This fundamental difference from energy-transportation wars is:

Energy shocks primarily reprice supply costs,

while sanctions-shocks primarily reprice settlement qualification.

Once settlement qualification fluctuates, asset rankings diverge rapidly. Assets heavily dependent on global banking, cross-border financing, and mainstream clearing networks tend to devalue; while new digital settlement tools capable of transferring, holding, or settling in restricted environments may gain extra attention.

IMF’s 2025 “Global Financial Stability Report” clearly states: major geopolitical risks, especially military conflicts, propagate through rising risk aversion, tightening financial conditions, and disrupted trade and financial links, significantly affecting equities, sovereign risk premiums, exchange rates, and commodities; major events can also sharply lower stock prices and elevate sovereign risk premiums. For markets, the focus of sanctions-payment wars isn’t “which asset will rise,” but whether financial intermediation can still function smoothly.

IMF’s research on geopolitical risks also shows that major military conflicts not only lower stocks and raise sovereign risk premiums via increased risk aversion and tighter financial conditions but also spill over through trade and financial links to third countries.

This is why sanctions-type shocks often spread farther than the battlefield itself.

For new on-chain settlement tools, a more precise statement isn’t “they are inherently safe,” but: when traditional payment frictions, capital flow restrictions, and cross-border settlement barriers rise, markets will reassess their role as non-bank, cross-border, 24/7 settlement channels. The real re-evaluation isn’t of some alternative store of value narrative, but of the institutional value of these settlement channels.

If energy-transportation war asks “Can goods get through,”

then sanctions-payment war asks:

Can the money still go through?

04 | Supply chain-physical conflict

“Markets trade profit and loss statements first, not safe-haven narratives.”

Another type of conflict neither directly blocks global energy arteries nor immediately rewires international payment systems, but still significantly alters asset pricing.

This is: supply chain-physical conflict.

The core isn’t about “the world will immediately enter full risk aversion,” but whether production, transportation, inventories, and delivery systems remain distorted.

It first rewrites variables closer to corporate operations: freight costs, insurance, delivery cycles, inventory safety margins, profit margins, and capital expenditure expectations.

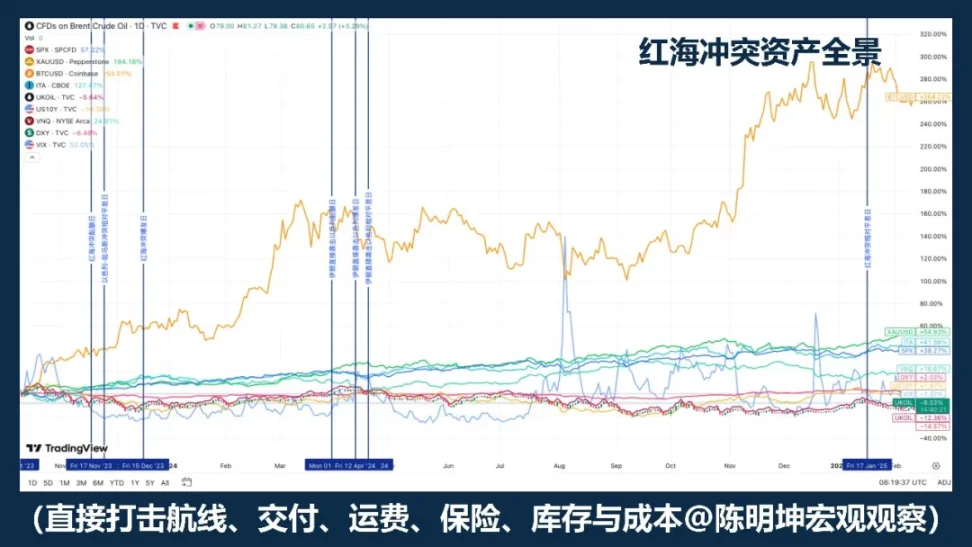

The most typical example is the Red Sea conflict. IMF reports that in the first two months of 2024, trade volume through the Suez Canal dropped about 50% year-over-year, and attacks forced many ships to reroute around the Cape of Good Hope, disrupting supply chains; UNCTAD also notes that by mid-February 2024, container throughput via the Suez had fallen 82%, with many ships diverting to Africa’s southern tip.

In this type of shock, the market’s first trades aren’t “buy safe-haven,” but: which costs will rise; whose deliveries slow; whose profit margins will be hit first; whose orders will migrate; and which companies’ substitution capacity will be revalued.

Its transmission chain isn’t a simple risk-off line, but a chain closer to the real economy:

Regional conflict escalation

→ Shipping and supply disruptions

→ Delivery cycles extend, inventory strategies adjust

→ Costs rise, margins compress, order flows diverge

→ Sector reordering within stocks, not a uniform risk-off

The most common misjudgment here is to conflate “conflict” with “safe-haven.”

But supply chain-physical conflicts don’t usually produce a uniform risk trade across the entire market initially.

More often, the result is:

Sector differentiation, profit divergence, regional disparity.

This explains why the impact of this type of war on assets is often slower but not necessarily smaller. The real impact usually manifests at three levels:

First, cost: shipping, insurance, warehousing, parts procurement, alternative routes increase costs.

Second, inventories: firms shift from efficiency to resilience.

Third, profitability: can companies still meet earnings forecasts? When it reaches this stage, conflicts begin to influence profit forecasts and valuation models.

Therefore, asset performance under this type of war isn’t about all assets risk-off together, but about internal sector re-pricing. Companies heavily dependent on specific regional capacities, single routes, or just-in-time, low-inventory models are more vulnerable; those with diversified capacities, regional spread, stronger pricing power, or order transfer ability may benefit.

So, a more accurate conclusion isn’t:

“Conflict comes, buy safe-haven,”

but:

When war first impacts production, transportation, inventories, and delivery systems, the market re-evaluates not all assets equally, but costs, margins, and industry rankings.

If energy shocks first reframe prices,

payment shocks first reframe qualification,

then supply chain shocks first reframe:

the profit and loss statement.

5. From judgment to position—investment methodology in war

Earlier, we discussed how war enters asset pricing.

But for investors, the more crucial question isn’t just understanding this,

but taking a step further:

How to translate judgments into positions.

The most common misconception about war is that it’s a huge directional opportunity.

But a careful review of history shows war doesn’t produce stable, repeatable directions.

Instead, it more reliably causes: volatility, mispricings, and correlation breakdowns.

Therefore, investing during war isn’t about betting on a direction,

but about first identifying which variables the market is trading:

Are these variables causing short-term pulses,

or propagating along the asset chain?

Which prices are just emotional reactions,

and which shocks will settle into medium-term trends?

To make this more concrete and actionable, I break it into four steps.

First, always identify the first-priority variable.

After war breaks out, the market won’t trade all information simultaneously. It will first latch onto one variable and push it into the pricing center: sometimes oil, sometimes risk appetite, sometimes settlement capacity, sometimes inventories and profit statements. Many people want to make a broad judgment about the entire war at once, but that’s usually too early and too coarse. The effective approach is to first judge:

What is the market trading right now—supply, risk appetite, settlement friction, or profit outlook?

Getting the first-priority variable right sets the direction for positions; getting it wrong means even with a complete narrative, trading will likely fail.

Second, prepare before the conflict erupts, not during.

Good war trades often don’t start at the moment of full-blown conflict. Many high-probability opportunities appear before the event enters public sentiment. By the time the market discusses it, the best entry window has often already passed.

So, pre-war preparation is key: study boundaries, develop tools, identify vulnerabilities, reserve hedges. Don’t wait for gunfire to decide what weapons to use.

Third, during conflict, shift to trading based on pricing deviations.

After war erupts, explanations are plentiful; what’s scarce is judgment of prices. War doesn’t have a one-size-fits-all asset template; instead, it tends to create upheaval.

Initially, markets often overreact or underreact, or assets move together driven by emotion. In other words, war often doesn’t produce a clear direction but amplifies mispricings temporarily.

This is why war isn’t always suitable for stable directional bets,

but often better for arbitrage and structural trades.

Because during upheaval, the first thing disrupted isn’t opinions,

but the order of prices that were previously stable:

Spot and derivatives may disconnect

Related assets may disconnect

Safe-haven narratives and actual prices may diverge

Short-term sentiment and medium-term transmission may misalign

During this phase, the most important isn’t to take a stance,

but to identify which prices are just emotional pulses, which mispricings will quickly revert, which shocks will settle into medium-term trends, and which spreads, basis, and correlations are worth trading.

This stage especially relies on arbitrage intuition and experience.

When you see war triggering certain asset moves, those who have studied historical samples can more quickly deploy strategies. For example, in the 2025 silver short squeeze, sharp traders can swiftly pursue silver arbitrage; similarly, recent gold fluctuations under the Israel-Hamas conflict make it easier for savvy traders to find pricing mismatches among different gold derivatives.

These opportunities come fast and disappear quickly.

For skilled traders, they are windows;

for less experienced traders, they often just pass by as fleeting waves.

Fourth, after the crisis ferments, shift trading focus from events to transmission.

In early war stages, markets trade the event itself; as it develops, markets trade the transmission results. The real determinant of whether a war’s short-term pulse evolves into a medium-term trend isn’t the number of news stories, but whether the shocks continue to penetrate deeper variables: inflation expectations, discount rates, corporate profits, settlement and financing conditions.

If these variables aren’t truly changed, the initial volatility is often just risk discounting, not a long-term revaluation; but if these variables do change, war ceases to be just news and begins to become part of a trend. At this stage, the trading logic must shift:

From event pulses to trend judgment,

From news-driven to macro mainline.

Macro hedging requires flexible tools. Facing different macro phenomena, war types, and transmission paths, traders must switch tools and enter different capital battlegrounds.

Ultimately, position isn’t an emotional accessory but a reflection of ideas expressed in capital.

War amplifies volatility and errors in judgment.

The purpose of positions is to allow ideas to be tested by the market.

Opinions must correspond to variables;

judgments must correspond to tools;

and logic must ultimately translate into capital allocation.

This is my understanding of war investment methodology:

Pre-war: analyze logic; during war: identify mispricings; post-war: observe transmission.

First, focus on variables; then on prices; finally, on positions.

Because positions make ideas falsifiable.

And investing is the shortest direct route from ideas to wealth.