Gold experienced its largest weekly decline since 1983 this week, with prices falling approximately $600 in just a few days. This sharp drop occurred during a period of intense geopolitical tensions, which traditional theory suggests should support gold. Analysts point out that the fundamental reason for this decline is not a collapse in safe-haven demand, but rather forced selling caused by liquidity tightening in overly crowded institutional positions, prompting smart money to reallocate.

Structural Explanation for the Gold Crash: Overcrowded Trades Meet Liquidity Crisis

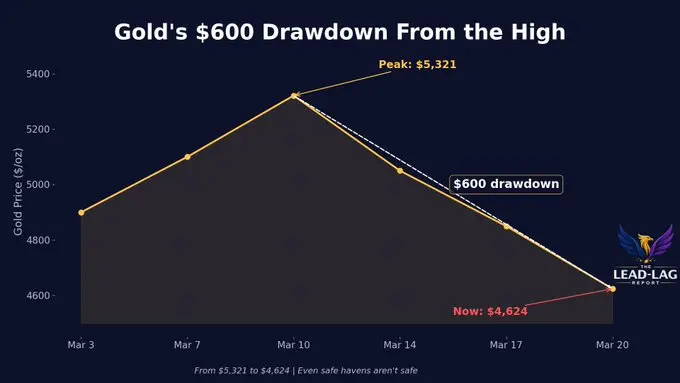

(Source: LeadLag Report)

Coin Bureau founder Nick Paklin directly highlights the core contradiction: “Gold just experienced its worst week since 1983. And it’s during a time of war. The $5,500 gold price isn’t driven by safe-haven demand, but by trading — extremely crowded trades.”

This phenomenon has structural roots. After Russia’s assets were frozen in 2022, central banks worldwide began large-scale gold purchases, prompting institutional follow-on and record ETF inflows. However, this trend is now reversing: war has forced central banks to use foreign exchange reserves instead of accumulating more, and Gulf oil-producing countries facing export restrictions may shift from buyers to sellers, weakening the original demand pillar.

Meanwhile, the U.S. 10-year Treasury yield has surged under triple pressure from inflation fears, hawkish central bank signals, and leveraged position liquidations, forcing institutional investors to rapidly reduce risk. According to Kobeissi Letter data, retail put-buying sentiment has soared to 52%, the highest since mid-2025.

Three Rotations of Smart Money

Private Markets: Family offices have significantly shifted toward private equity, private credit, and other non-public assets. Senior family office professional Jack Claver states, “Family offices are no longer wasting time on basic stocks and bonds; the real returns are hidden there.” Due to their opaque pricing and low correlation with public markets, private markets are becoming increasingly attractive during this liquidity crisis.

Emerging Markets: Claver also notes that funds are flowing into emerging markets, seen as channels offering more attractive long-term growth potential amid overvalued developed markets (Berkshire Hathaway’s index at about 220% of GDP).

Digital Assets: Cryptocurrencies are re-entering the smart money’s allocation radar. Analyst Chad Stangerber points out that as gold declines, “capital rotation will begin toward other asset classes,” and believes cryptocurrencies are “still undervalued.”

Cryptocurrencies: Potential Beneficiaries After Forced Liquidations

Digital assets exhibit a dual nature in the current environment: during a “sell first, exchange later” phase, major cryptocurrencies like Bitcoin, which correlate about 89% with the S&P 500, have not escaped passive selling; however, many analysts believe that once forced deleveraging by institutions is complete, cryptocurrencies—due to their low entry barriers, 24-hour liquidity, and lower long-term correlation with traditional finance—may become a priority for capital reallocation.

Market dynamics suggest that the worst week in 43 years for gold has not only broken price levels but also shattered the market psychology that “geopolitical turmoil automatically equals gold rising.” This indicates that the next safe-haven narrative may need to be built on different assets.

FAQs

Q: Why does gold plummet during geopolitical crises?

This decline is mainly due to liquidity-driven forced selling, not investors actively abandoning gold. After the Russia-Ukraine conflict, central banks’ large gold purchases prompted institutional follow-on, creating overcrowded trades. When war forces countries to use foreign reserves and U.S. Treasury yields spike, triggering leverage unwinding, institutions prioritize selling their most profitable positions—precisely gold.

Q: What specific assets are institutional investors like family offices shifting toward?

According to reports, these institutions are moving toward three main areas: private equity and private credit markets (seeking uncorrelated returns), emerging markets (more attractive valuations), and digital assets (expected beneficiaries after capital rotation).

Q: Does the 43-year worst weekly decline in gold mean the end of its long-term investment case?

There is no definitive conclusion yet. The recent drop mainly reflects a short-term liquidity reset rather than a fundamental breakdown of gold’s long-term safe-haven logic. Some analysts believe that once forced selling ends, gold could still benefit from central banks’ diversification needs, but market structure stabilization is necessary to confirm this.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.