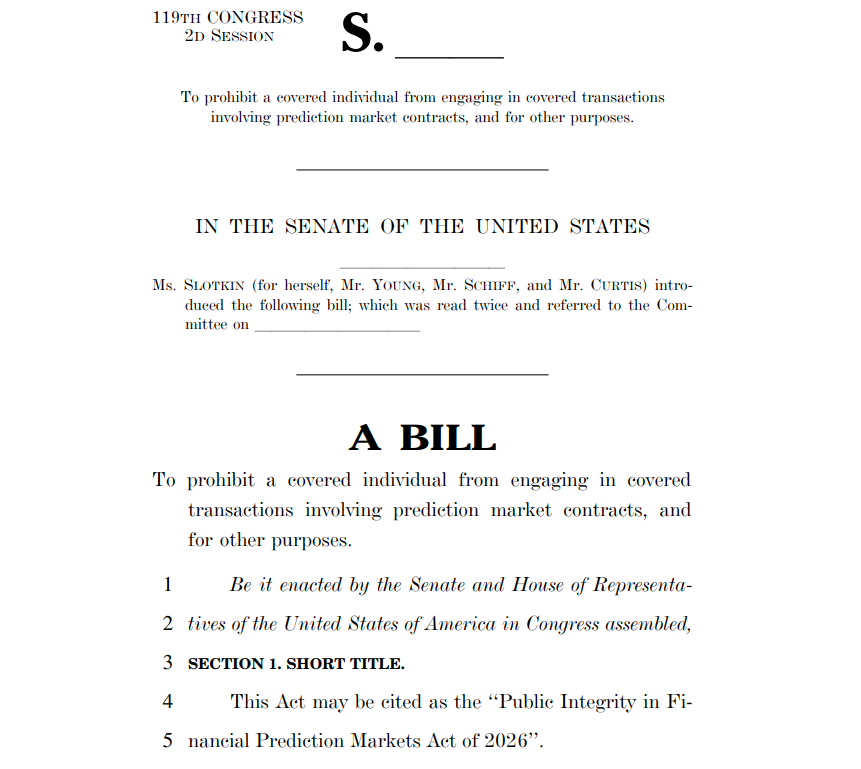

On March 26, bipartisan lawmakers in the United States jointly introduced the “2026 Financial Prediction Market Public Integrity Act,” which has been submitted to the 119th Congress’s second session. The bill aims to prohibit government officials from using undisclosed insider information to bet on prediction market contracts, with a fine mechanism of up to twice the profit gained, and requires officials to declare all bets over $250 within 30 days, covering the President, Vice President, all members of Congress, and political appointees.

Broad Applicability of the Bill and New Definition of “Insider Information”

(Source: John Curtis)

(Source: John Curtis)

The “2026 Financial Prediction Market Public Integrity Act” sets a broad regulatory scope regarding its subjects of applicability:

Executive Branch: The President, Vice President of the United States, and employees of executive agencies or independent regulatory bodies

Legislative Branch: All members of the Senate and House of Representatives

Political Appointees: All individuals in political positions appointed by the President

The bill also provides a clear definition of “insider information”: any “information that a rational investor would consider important and is not publicly disclosed when making decisions related to prediction market contracts” is governed by this act, which has a broader definition than the insider trading standards in traditional securities law. This means that even atypical government information may be subject to restrictions.

Reporting Mechanism and Penalty Provisions: $250 Threshold and Double Profit Penalty

The bill sets specific provisions regarding reporting and penalties. Any government official who bets over $250 on prediction markets must submit a report to the Office of Government Ethics within 30 days, including the number of contracts purchased, contract price, transaction date and time, contract name, contract position, the name of the trading platform used, and the profit and loss status of the transaction.

Violators will face a civil penalty of $500 or twice the profit gained from the prediction market contract—whichever is higher. This “double profit” penalty is designed to fundamentally eliminate the financial incentive to profit from public office information.

Senator Slotkin stated in the bill’s announcement: “No one should profit from the information and knowledge gained from public office; this is absolutely not acceptable. This bill is an important first step in establishing common-sense rules for prediction markets, with real deterrent effects, ensuring that those who violate the regulations face real consequences.”

Legislative Context: This Week’s Density of Legislation Indicates a Trend Towards Stricter Regulation

This proposal is the second legislation this week targeting insider trading issues in prediction markets. On Tuesday, Representatives Adrian Smith and Nikki Budzinski introduced the “PREDICT Act,” which focuses primarily on bets related to political events, policy decisions, and government actions; the “Public Integrity Act” on Thursday expands the regulatory scope with a broad definition of “insider information” and provides more specific reporting mechanisms and penalty standards.

The intensive introduction of these two bills reflects the rising regulatory attention to prediction markets at both the federal and state levels in the United States. Major platforms like Kalshi and Polymarket have also proactively tightened their internal rules, restricting betting activities by political candidates and professional athletes on their platforms, indicating that the industry is actively adjusting in line with regulatory expectations.

Frequently Asked Questions

What are the core prohibitions of the “2026 Financial Prediction Market Public Integrity Act”?

The bill prohibits the President, Vice President, members of Congress, political appointees, and employees of executive agencies from betting on prediction market contracts using “undisclosed information that a rational investor would consider important.” Its definition of insider information is broader than that of traditional securities law, covering non-public information in the government decision-making process.

What are the main differences between this bill and the “PREDICT Act” introduced on Tuesday?

The “PREDICT Act” focuses specifically on prediction market bets related to political events, policy decisions, and government actions; the “Public Integrity Act” adopts a broad definition of “insider information” while also establishing specific reporting mechanisms (reporting bets over $250 within 30 days) and clear penalty standards (up to double profits), making its regulatory framework more comprehensive.

What must government officials report, and what consequences will they face for violations?

Bets over $250 on prediction markets must be reported to the Office of Government Ethics within 30 days, including the number of contracts, prices, platform names, and profit and loss status. Those who fail to report as required or engage in illegal betting will face a penalty of $500 or double the profit gained, whichever is higher.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.