XWIN Research’s latest analysis published on CryptoQuant Insights indicates that in Q1 2026, Bitcoin has not “gone extinct,” but is instead undergoing a structural supply shift: the exchange whale ratio continues to rise, signaling that native crypto large holders are selling; at the same time, publicly listed companies led by MicroStrategy added approximately 62,000 BTC net in the same period, indicating a bidirectional transfer of “whales out, companies in.”

The core evidence of market bifurcation: synchronous coexistence of sellers and accumulators

The exchange whale ratio is a key metric for measuring large capital inflows to exchanges; when it rises, it usually means major holders with large amounts of Bitcoin are preparing to sell. In Q1 2026, this indicator continued to climb, effectively suppressing each attempt by Bitcoin to break through the $70,000 resistance level in a low-liquidity environment.

However, corporate-side actions starkly contrast with this. XWIN Research estimates that public companies added roughly 62,000 BTC net in the first quarter; Strategy currently holds about 762,000 BTC, with funding sources including convertible bonds and stock issuance—its buying strategy is completely unaffected by short-term price swings.

The analysts’ core point is: even if Bitcoin’s price hovers below $70,000, companies’ ongoing buying is quietly shrinking the market’s available supply, though this effect has not yet been fully reflected in price action.

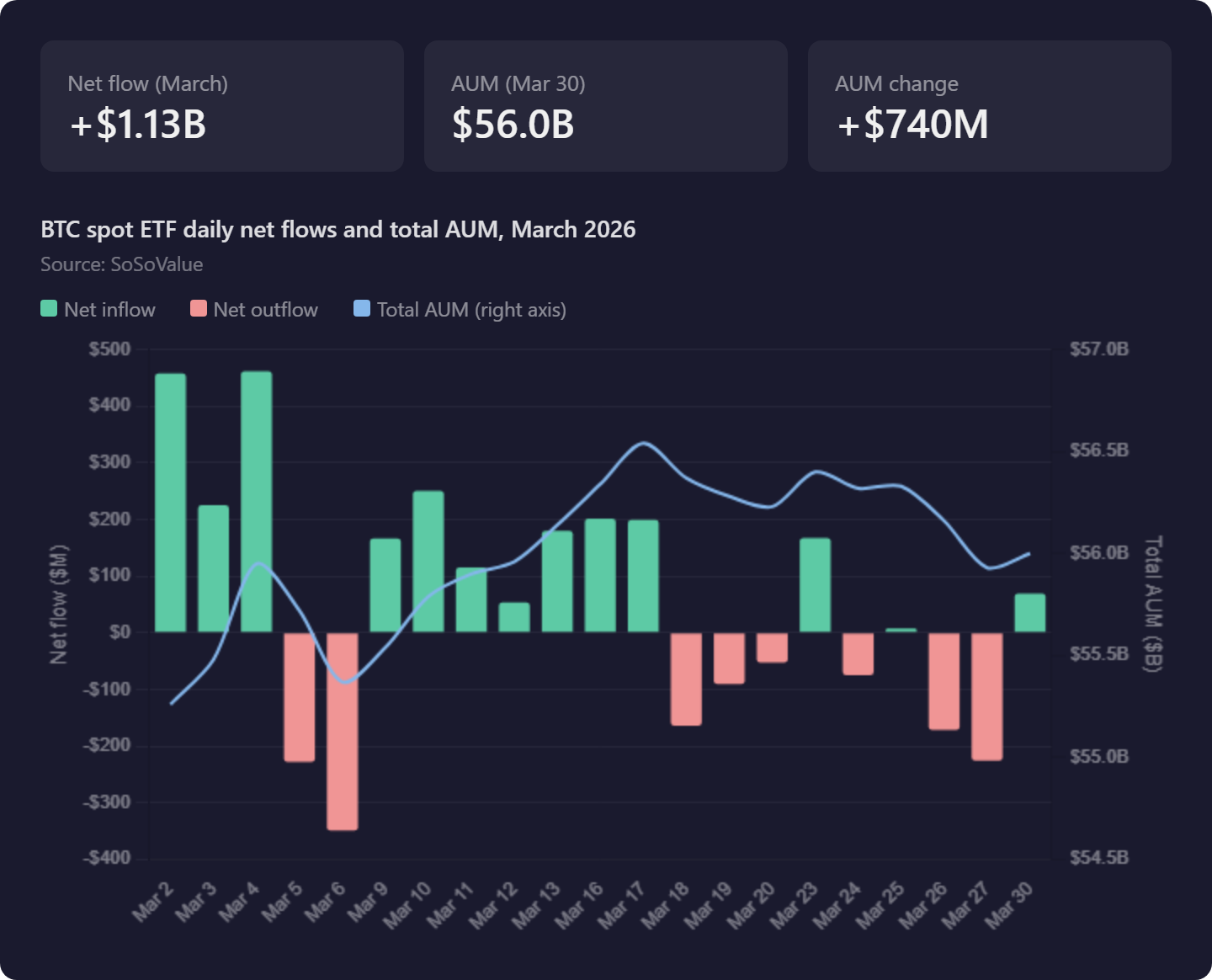

Spot ETFs: rotation rather than net increases, with BlackRock continuing to absorb while Grayscale keeps bleeding

(Source: SoSoValue)

Fund flows into spot Bitcoin ETFs add another layer of complexity to the market. Here are the key flow figures for the quarter:

March 2: ETF market posted net inflows of $458 million on a single day; short-term institutional sentiment clearly warmed up

March 6: Just four days later, the market reversed course and saw net outflows of $348 million

Full-quarter AUM performance: up only from $55.26 billion at the start of the year to $56 billion by the end of March—almost flat

The internal rotation at the core: BlackRock continues to receive net inflows; Grayscale (GBTC) continues to face redemptions

XWIN Research’s conclusion is: this is the redeployment of existing assets by institutional investors across different Bitcoin products, rather than new external capital entering the Bitcoin ecosystem. Until net inflows and outflows show continuous and significant improvement, ETFs are more like a neutral presence for Bitcoin—not an outright bullish active catalyst.

The supply-shift hypothesis: early whales are orderly exiting, enabled by corporate buy demand

XWIN Research’s most thought-provoking conclusion concerns the long-term evolution of market structure. Early long-term holders that bought Bitcoin at prices far below today’s market level are now facing steady demand from companies like Strategy that keep entering regardless of whether prices are high or low. This creates an exit window similar to an IPO timing—allowing them to reduce positions in an orderly way without severely shaking the market.

Bitcoin’s supply hasn’t disappeared; it has simply been transferred in large scale from decentralized early adopters to companies’ balance sheets. Analysts note that companies such as Strategy are gradually replacing native crypto whales as the market’s primary destination for long-term supply absorption—they have the financing capacity of traditional capital markets, making them more persistent and more leveraged buyers than early crypto whales.

Frequently Asked Questions

Why doesn’t an increase in the exchange whale ratio equate to a bearish confirmation?

An increase in the exchange whale ratio does indicate that large holders are moving funds to exchanges (usually for selling), which increases selling pressure in the short term. But XWIN Research points out that if these sell orders simultaneously meet sustained counterpart buy demand from companies like Strategy, the net effect may be that supply is redeployed among higher-quality long-term holders rather than dropping overall; the key lies in the relative scale of the two forces.

If ETF AUM is barely growing, does it mean institutional demand is weakening?

If ETF AUM growth mainly comes from internal rotation of Grayscale flows to BlackRock, then yes—it would mean no new external capital is entering the Bitcoin market. What truly represents demand expansion is sustained net inflows; and the current data more reflects institutional preference shifts across different Bitcoin products, with limited impact from any real increase in total long-term holdings.

What is the most crucial indicator to watch for Bitcoin’s price action in Q2?

Analysts believe the core proposition for Q2 is: can sustained corporate buying withstand whale selling pressure for long enough time to wait for broader demand to follow? Key indicators include: whether ETF monthly net inflows show a sustained positive turn; the pace at which companies—led by Strategy—add positions; and whether the exchange whale ratio tops out and then pulls back—none of the three can be missing.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.