Amid the wave of billions of USD in ETF capital continuously flowing in, the group of mid-cap companies in Asia is emerging as a new structural demand for the circulating supply of Bitcoin.

In Japan, Metaplanet has held over 30,000 BTC on its balance sheet, while South Korea's Bitplanet has launched a supervised Bitcoin accumulation program in compliance with the country's first regulation.

Discrete pilot projects such as Nexon's Bitcoin purchase in 2021 or Meitu's brief investment have now transitioned into a stage of strategic accumulation and standardization.

Metaplanet – originally a hotel company – has transformed into a Bitcoin treasury business, announcing monthly BTC purchase reports and raising funds with the sole aim of expanding its holdings.

Bitplanet, after rebranding from SGA Solutions, has become the first company in South Korea to implement a managed corporate Bitcoin purchasing program, aiming for a target of 10,000 BTC through daily purchases.

Meanwhile, smaller enterprises in the region are striving to join the mid-cap group. Thailand's DV8 has completed the first step in its strategy to transition its treasury to crypto, raising 7.4 million CAD through a stock purchase rights.

In Hong Kong, AsiaStrategy and HK Asia Holdings are repositioning as listed vehicles for corporate exposure to Bitcoin.

- AsiaStrategy ( was previously a luxury retailer Top Win International) now allocates part of its treasury to Bitcoin and accepts BTC in payments, aiming to achieve a holding value of 1 billion USD.

- HK Asia Holdings is also implementing a Bitcoin-denominated treasury model, having purchased 28.9 BTC in 2025, according to the “MicroStrategy for Asia” framework proposed by Sora Ventures.

The question is no longer whether businesses will buy Bitcoin, but rather whether the mid-cap group in Asia can absorb enough new supply to tighten the circulating amount as ETF demand rises sharply.

If the current pace is maintained, the total amount of net BTC purchased by this group could be equivalent to, or even significantly exceed, the amount issued by miners – adding another layer of bridge alongside the ETF.

Japan and South Korea lead the wave

Japan dominates this group with Metaplanet – a company that started its Bitcoin treasury strategy in December 2024 and is accelerating rapidly in 2025.

- From 2,100 BTC in February, the number has reached 30,823 BTC by the end of September, placing Metaplanet in the top 4 largest Bitcoin holders globally.

- The company announced “Phase II: Bitcoin Platform” – a long-term fundraising strategy to continue accumulation.

Nexon, the “giant” game listed in Tokyo, purchased 1,717 BTC in April 2021 at an average price of 58,226 USD/BTC and has held it until now.

In South Korea, Bitplanet emerged in Q4/2025 with its first purchase of 93 BTC under national supervision. The company aims for 10,000 BTC, with a purchasing program that complies with transparency rules.

Conversely, Meitu in Hong Kong is a reverse example – the company sold all of its BTC and ETH by the end of 2024, highlighting the difference between a temporary experiment and a sustainable treasury strategy.

The ability to absorb supply

Only Metaplanet in 2025 has purchased an additional 28,723 BTC – equivalent to 64 days of new issuance ( based on the rate of 450 BTC/day after halving ).

In total, this figure accounts for about 20% of the Bitcoin issued since the beginning of (, estimated at around 136,000 BTC).

Compared to the ETF, in October 2025, Bitcoin exchange-traded funds recorded 3.55 billion USD and 921 million USD in inflows during two peak weeks – equivalent to tens of thousands of BTC each week.

This means that the amount of BTC that Metaplanet purchases in a year is roughly equivalent to one week of strong ETF, but the important difference is: the company's buying program is long-term and rule-based, not dependent on market emotions.

If this pace is maintained, the Asian mid-cap group could absorb 20-30% of the monthly issuance, before considering the US companies that may participate once the policy is clearer.

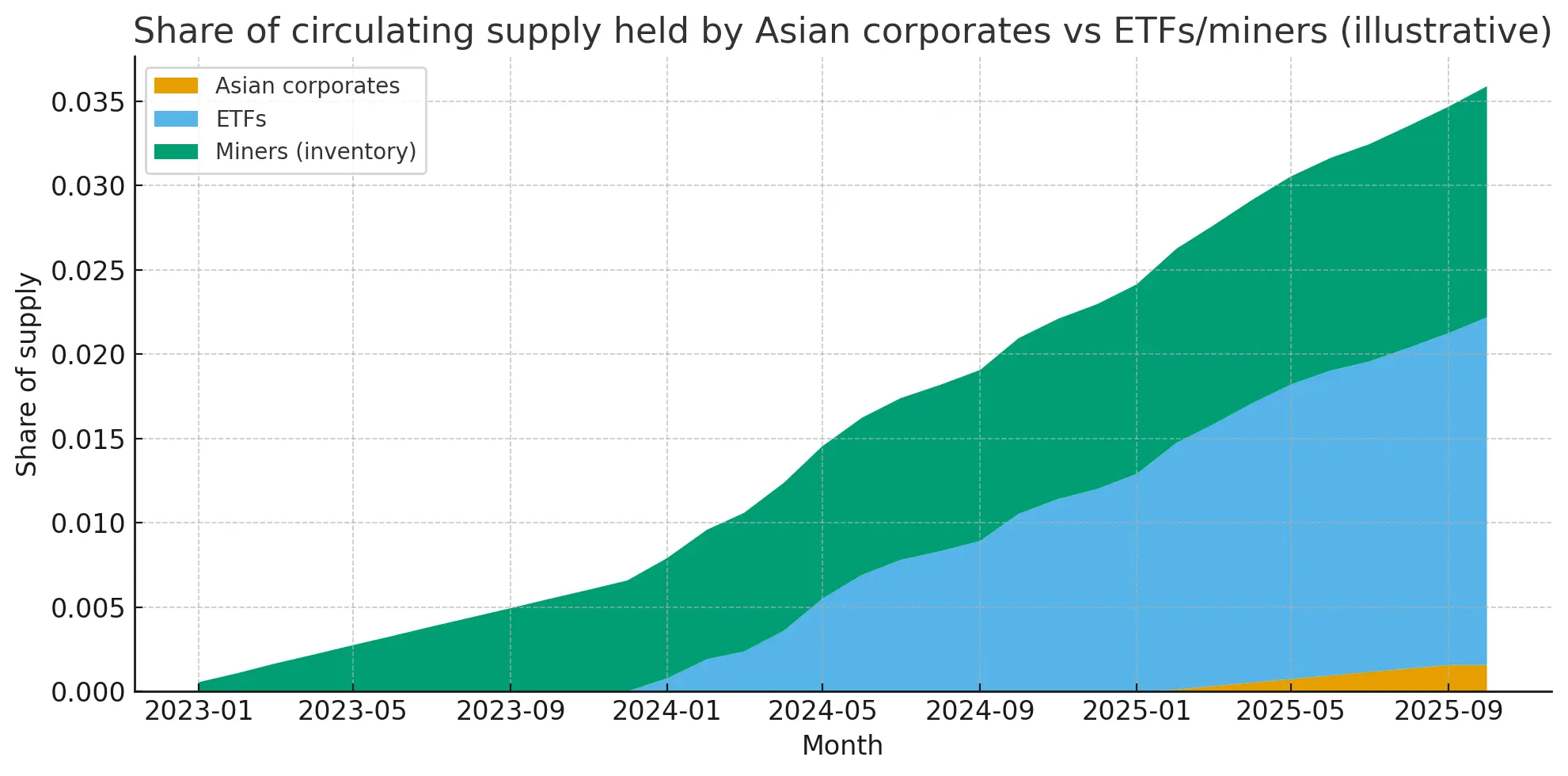

The percentage of circulating supply held by Asian corporations has increased from nearly 0 at the beginning of 2023 to about 0.2% by the end of 2025, following ETF funds and the inventory of mining companies.### Risks: accounting, custody, and governance

The percentage of circulating supply held by Asian corporations has increased from nearly 0 at the beginning of 2023 to about 0.2% by the end of 2025, following ETF funds and the inventory of mining companies.### Risks: accounting, custody, and governance

The major difference lies in the standards of disclosure and auditing.

- Metaplanet announces regularly but has not disclosed details about costs or custody partners.

- Bitplanet complies with South Korean regulations but the official DART report has not yet appeared.

- Nexon publicly disclosed the initial buying price but has not provided further updates.

Governance risks are also notable: decisions are largely driven by the founders and may be reversed if there is a change in personnel or shareholder pressure.

For example, Meitu quickly withdrew when crypto became a burden instead of an asset.

The legal framework for custody in Japan is gradually improving but is still less developed than in the US; in South Korea, supervision helps increase transparency but makes businesses dependent on policies.

Changes in taxes, accounting, or regulations remain a “black swan” factor that could slow down the accumulation.

Looking towards 2026 and beyond

Analysts will closely monitor how Metaplanet implements its fundraising strategy “Phase II”, as well as the DART progress of Bitplanet confirming the target of 10,000 BTC.

If the Asian mid-cap group maintains a buying pace of 5,000–10,000 BTC each month in 2026, they could absorb 11–22% of the new supply, creating a noticeable impact on the supply-demand structure along with the ETF.

If failure is due to governance, policy risks, or capital costs, the argument about “the bridge of business structure” will weaken, bringing Bitcoin back into the orbit dependent on ETF and retail investors.

Conversely, if successful, Metaplanet and Bitplanet could pave the way for an “Asian version of MicroStrategy” – and by the halving in 2028, the market will face a new layer of bridge: global corporate treasuries systematically accumulating Bitcoin, alongside ETFs and miners.

Vương Tiễn