UBS’s latest in-depth report rebuts the AI bubble narrative, noting that global data centers have 25GW of capacity under construction and existing capacity of 105GW, with vacancy rates at record lows. UBS has raised its 2026 market growth forecast to 20-25%. Annualized recurring revenue from generative AI has reached $1.7 billion, with enterprises seeing a 3.6% increase in revenue and a 5% reduction in costs through AI adoption.

Supply-Demand Imbalance Proves Genuine Demand

(Source: UBS)

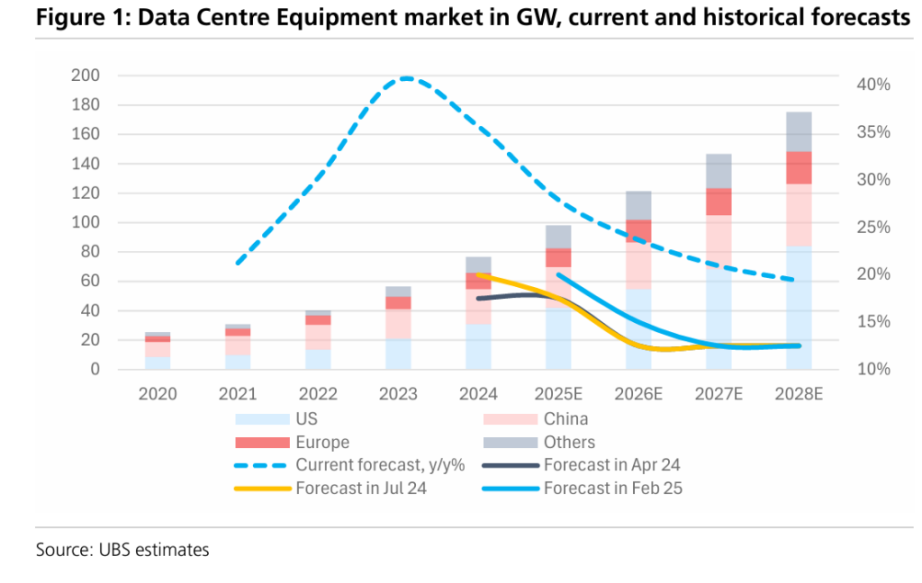

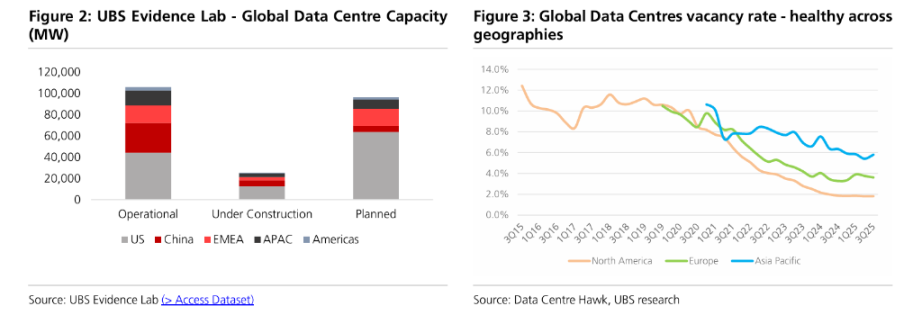

UBS Evidence Lab monitoring data shows that global data center capacity is in a period of rapid expansion. Vacancy rates in North America, Europe, and Asia-Pacific are 1.8%, 3.6%, and 5.8% respectively—historical lows, indicating a supply-constrained market. Analyst Andre Kukhnin’s team notes that even without factoring in new projects, if only the planned capacity comes online as scheduled by 2029, the compound annual growth rate for 2025-2029 will reach 21%.

This supply-demand imbalance directly rebuts the AI bubble argument. A bubble is characterized by oversupply and false demand, but the current record-low vacancy rates in data centers prove that demand is real and persistent. UBS expects market growth of 25-30% in 2025, 20-25% in 2026, 15-20% in 2027, and steady growth of 10-15% during 2028-2030.

Monetization Data Shatters Bubble Narrative

(Source: UBS)

The issue investors care most about—“return on investment”—has received early positive evidence from UBS. The annualized recurring revenue of major AI-native applications has reached $1.7 billion, accounting for about 6-7% of the current SaaS market total. According to the latest McKinsey survey, in the past 12 months, enterprises achieved an average revenue increase of 3.6% and an average cost reduction of 5% through AI.

The core argument of the AI bubble theory is “huge investment but no monetization,” but the $1.7 billion ARR shows that monetization is already emerging. UBS emphasizes that GenAI, as a technology, is being adopted at an unprecedented rate—completely different from the dot-com bubble era, when technology was immature and application scenarios unclear.

Liquid Cooling Technology Leads with 45% Growth Rate

(Source: UBS)

As AI chip power density increases, the cooling market stands out. UBS expects the cooling segment to maintain about a 20% compound annual growth rate by 2030, with liquid cooling technology leading the way at a 45% growth rate, making it the fastest-growing sub-sector. This explosive growth in technical demand further proves the reality of AI infrastructure investment.

The construction cost of AI data centers is undergoing structural change. Compared to traditional data centers, facility costs per megawatt for AI data centers are up about 20%, but more critically, IT equipment costs have surged—due to expensive AI chips, IT equipment now accounts for a much higher proportion of total costs, with per-megawatt costs 3-4 times higher than traditional setups. This structure makes customers less sensitive to facility-side pricing, benefiting upstream equipment suppliers.

Power Bottlenecks Drive Up Asset Values

UBS also highlights potential risks. Power supply is seen as the biggest bottleneck—especially in Europe, where grid connection schedules for some primary hubs have been pushed back to the 2030s. UBS expects data centers to account for over 60% of incremental US power demand from 2025-2030, posing a challenge to grid reliability.

However, in UBS’s view, these bottlenecks mostly drive up the value of existing assets rather than ending the investment cycle. This is the opposite of bubble-burst logic—when a bubble bursts, asset values collapse, but current bottlenecks actually strengthen scarcity premiums. While hyperscale cloud providers’ capital expenditures account for 25-30% of sales, they still represent 75% of operating cash flow and remain manageable. This high level of investment is expected to continue at least through 2027.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.