This report is authored by Tiger Research. What if bridging assets could be put to use? We deeply analyze Katana, an ever-sleeping blockchain. It reinvests 100% of on-chain and off-chain yields and transaction fees into DeFi.

Key Points

- Most Layer 2s lock bridging assets without utilizing them. Katana deploys these assets into Ethereum lending protocols to generate yields, then redistributes the earnings as DeFi protocol incentives.

- Storing assets in a vault yields no returns. Users must deploy capital into Katana’s DeFi protocols to earn additional rewards.

- By Q3 2025, over 95% of Katana’s TVL is actively deployed in DeFi protocols. This contrasts with most chains, whose utilization rates range from 50% to 70%.

- Katana reinvests 100% of net sequencer fee income into liquidity provision, maintaining stable trading conditions even during market volatility.

1. Why is capital idle?

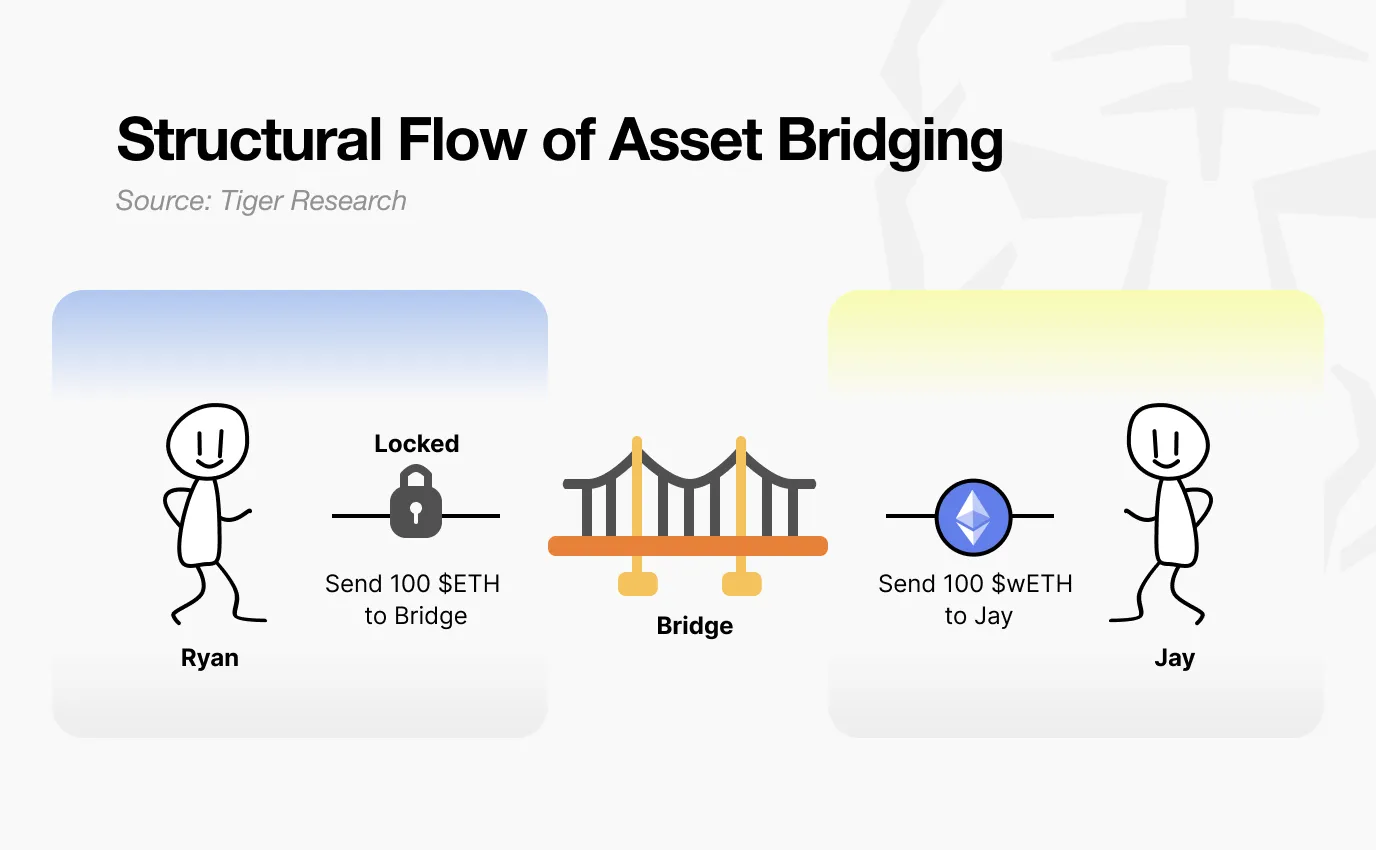

What happens to your funds when you cross-chain from Ethereum to Layer 2?

Source: Tiger Research

Most people think their assets are just transferred. In reality, the process is closer to freezing. When you deposit assets into a bridge contract, the contract holds them in custody. Layer 2 mints equivalent tokens. You can trade freely on Layer 2, but your original assets on the mainnet remain locked and idle.

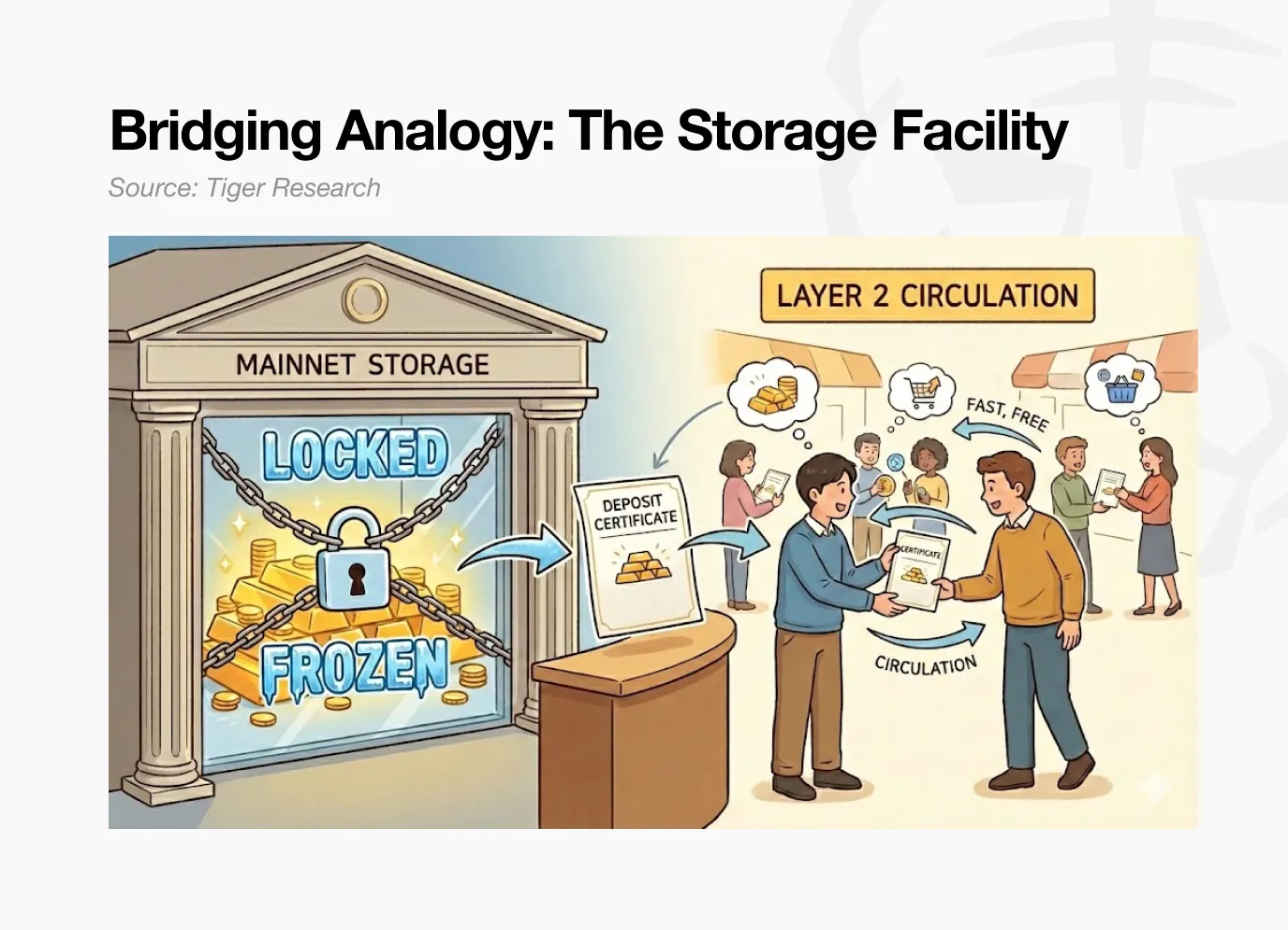

Source: Tiger Research

Consider a simple analogy. You store items in a storage facility and receive a withdrawal voucher. This voucher can be transferred to others. But the items themselves stay in storage until you retrieve them.

This describes how most Layer 2 bridges work. Assets held in Ethereum custody contracts generate no yield. They passively wait until users withdraw them back to the mainnet.

What if bridge deposits on the mainnet could earn DeFi yields, while you still enjoy fast, low-cost transactions on Layer 2?

Katana directly answers this question. Capital that enters the bridge is not idle. It is put to work.

2. How does Katana make capital work?

Katana activates capital through three mechanisms:

- Cross-chain assets are deployed into Ethereum lending markets to earn interest.

- Transaction fee income is reinvested into liquidity pools.

- Native stablecoin AUSD earns US Treasury yields.

External capital is in motion, and on-chain generated capital is also working. These three mechanisms together eliminate idle assets on Katana.

2.1. Vault Bridge

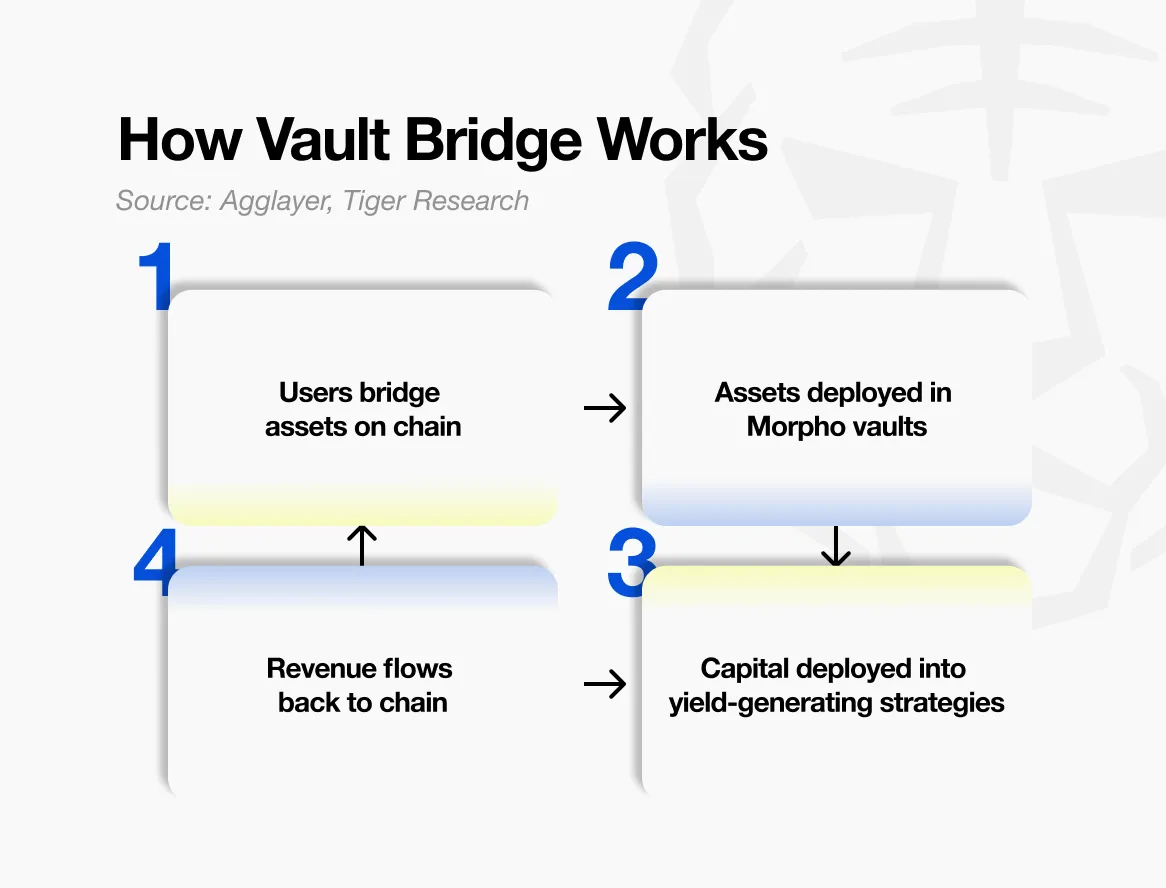

The first mechanism is Vault Bridge. When users send assets to Katana, the original assets remaining on Ethereum are deployed into lending markets to accrue interest.

Source: Agglayer, Tiger Research

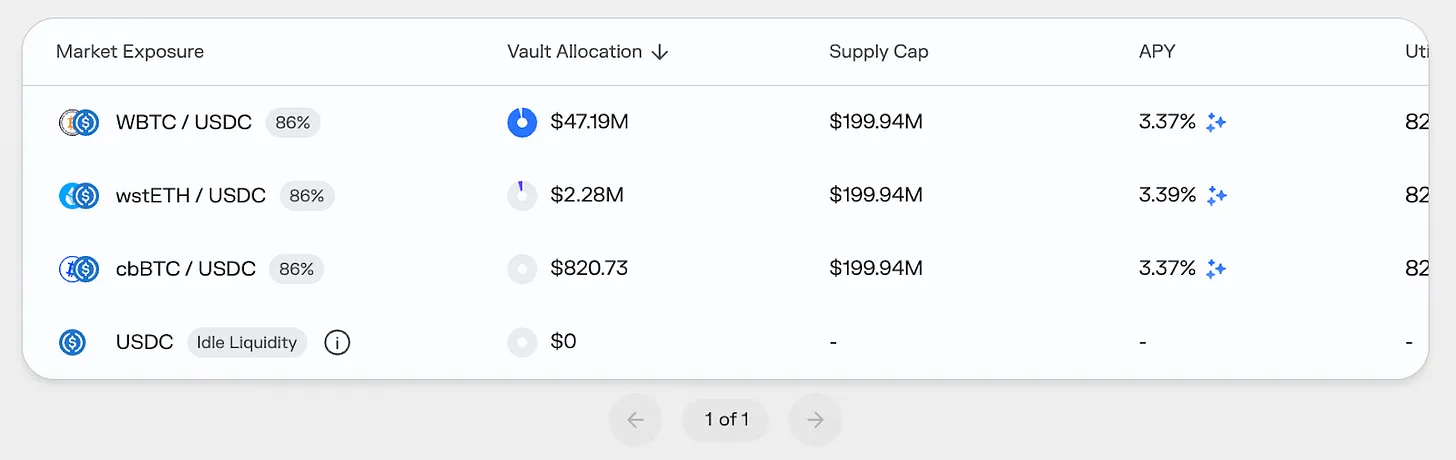

When you cross-chain USDC from Ethereum to Katana, these assets are not simply locked. On Ethereum mainnet, they are deployed into selected vault strategies of Morpho (a mainstream lending protocol). The generated yields are not directly distributed to individual users but are collected at the network level and redistributed as rewards to core DeFi markets on Katana.

On Katana, users receive corresponding vbTokens, such as vbUSDC. These tokens can be freely used within Katana’s DeFi ecosystem.

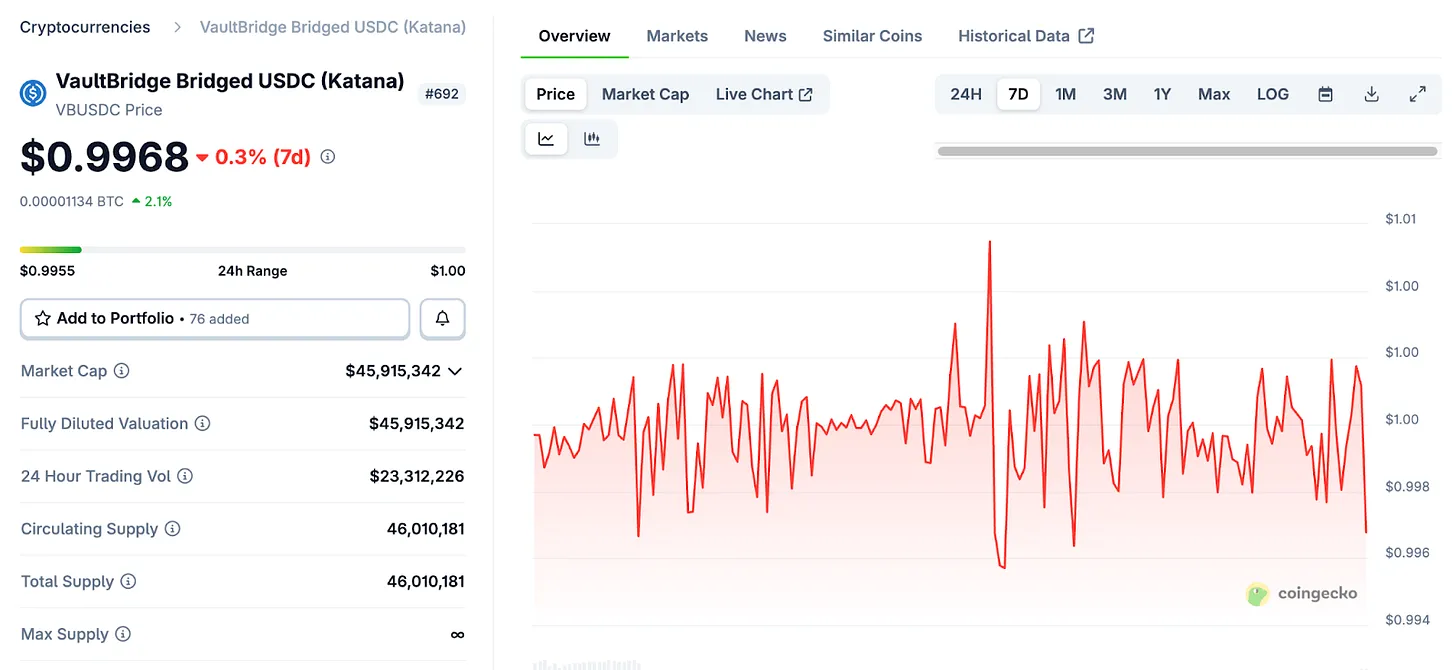

It’s important to clarify a common misconception. vbTokens cannot be compared to stETH or other staking derivatives. stETH appreciates automatically as staking rewards accrue.

Source: Coingecko

The mechanism of vbTokens is entirely different. Holding vbUSDC in a wallet does not increase the quantity or price. The yields generated by Vault Bridge on Ethereum do not flow to individual vbToken holders but go into Katana’s DeFi liquidity pools. These earnings are periodically distributed to the network to strengthen incentives for Sushi liquidity pools and Morpho lending markets.

Only active deployment of vbTokens benefits users. By staking vbTokens into Sushi liquidity pools or lending strategies on platforms like Yearn, users earn base yields plus additional rewards from Vault Bridge. Holding vbTokens passively yields no returns.

Katana rewards active utilization of assets, not passive holding. Capital that is active gets rewarded; idle capital does not.

2.2. Chain-Owned Liquidity (CoL)

The second mechanism is Chain-Owned Liquidity (CoL). Katana collects 100% of net sequencer fee income (transaction processing fees minus Ethereum settlement costs).

The foundation uses this income directly to become liquidity providers, supplying assets to Sushi trading pools and Morpho lending markets. This liquidity is owned and managed by the chain itself.

This creates a self-reinforcing cycle. As users trade on Katana, sequencer fees accumulate. These fees are converted into chain-owned liquidity, further deepening the pools. Slippage decreases, lending rates stabilize, and user experience improves. Better experience attracts more users, generating more fees. The cycle continues.

In theory, this structure is especially effective in a downtrend. External liquidity is highly mobile and can withdraw quickly under market pressure. In contrast, chain-owned liquidity is designed to remain in place, allowing the pools to operate continuously and absorb market shocks more effectively.

In practice, this sets Katana apart from most DeFi systems that rely on token issuance to incentivize external capital. By directly maintaining its own liquidity, the network aims for more stable and sustainable operations.

2.3. AUSD US Treasury Yield

The third mechanism is AUSD, Katana’s native stablecoin. AUSD is backed by US Treasuries, whose off-chain holdings generate yields flowing into the Katana ecosystem.

Source: Agora

AUSD is issued by Agora. The collateral backing AUSD is invested in physical US Treasuries. The interest from these bonds accumulates off-chain and is periodically transferred into the Katana ecosystem to strengthen incentives for pools denominated in AUSD.

If Vault Bridge brings on-chain yields, then AUSD brings off-chain yields. These two income sources are fundamentally different. Vault Bridge yields fluctuate with Ethereum DeFi market conditions, while AUSD yields are linked to US Treasury rates and are relatively stable.

This diversification of Katana’s revenue structure provides a buffer during on-chain market volatility; when on-chain yields are low, off-chain bond returns support overall income. This structure bridges the crypto market and traditional finance.

3. Locking Capital vs Making Capital Work

As previously mentioned, most existing cross-chain bridges choose simple asset locking for safety reasons. When assets are not moved, system design remains simple, and attack surfaces are limited. Most Layer 2 networks adopt this approach. While secure, capital remains idle.

Katana takes the opposite stance. Activating idle assets introduces additional risks, and Katana is very transparent about this trade-off. The network does not avoid risk but collaborates with mature risk management firms in DeFi, including Gauntlet and Steakhouse Financial.

Source: DefiLlama

Gauntlet and Steakhouse Financial are experienced risk management institutions in DeFi, with expertise in setting parameters for mainstream lending protocols and advising top DeFi projects. Their roles are similar to traditional asset management firms, responsible for evaluating where to allocate capital, determining appropriate position sizes, and continuously monitoring risk exposure.

Source: Morpho

No financial system can guarantee 100% safety, so concerns about residual risks are reasonable.

However, Katana works with top risk management firms and maintains a conservative vault architecture. An internal risk committee oversees operations. Additional security measures include multiple protections such as liquidity buffers provided by Cork Protocol.

4. Katana’s DeFi Ideal Country

The current DeFi market faces liquidity fragmentation. Funds for trading the same assets are spread across different chains and protocols, reducing execution efficiency, increasing slippage, and lowering capital utilization. Some users profit from arbitrage in these inefficiencies, but most have to bear higher costs.

Katana addresses this issue at the system level.

Vault Bridge and chain-owned liquidity concentrate liquidity into core protocols. The result: improved trade execution efficiency, reduced slippage, and more stable lending rates. Most importantly, yields from idle assets on Ethereum mainnet are added to the base yields, increasing overall returns.

Source: Morpho

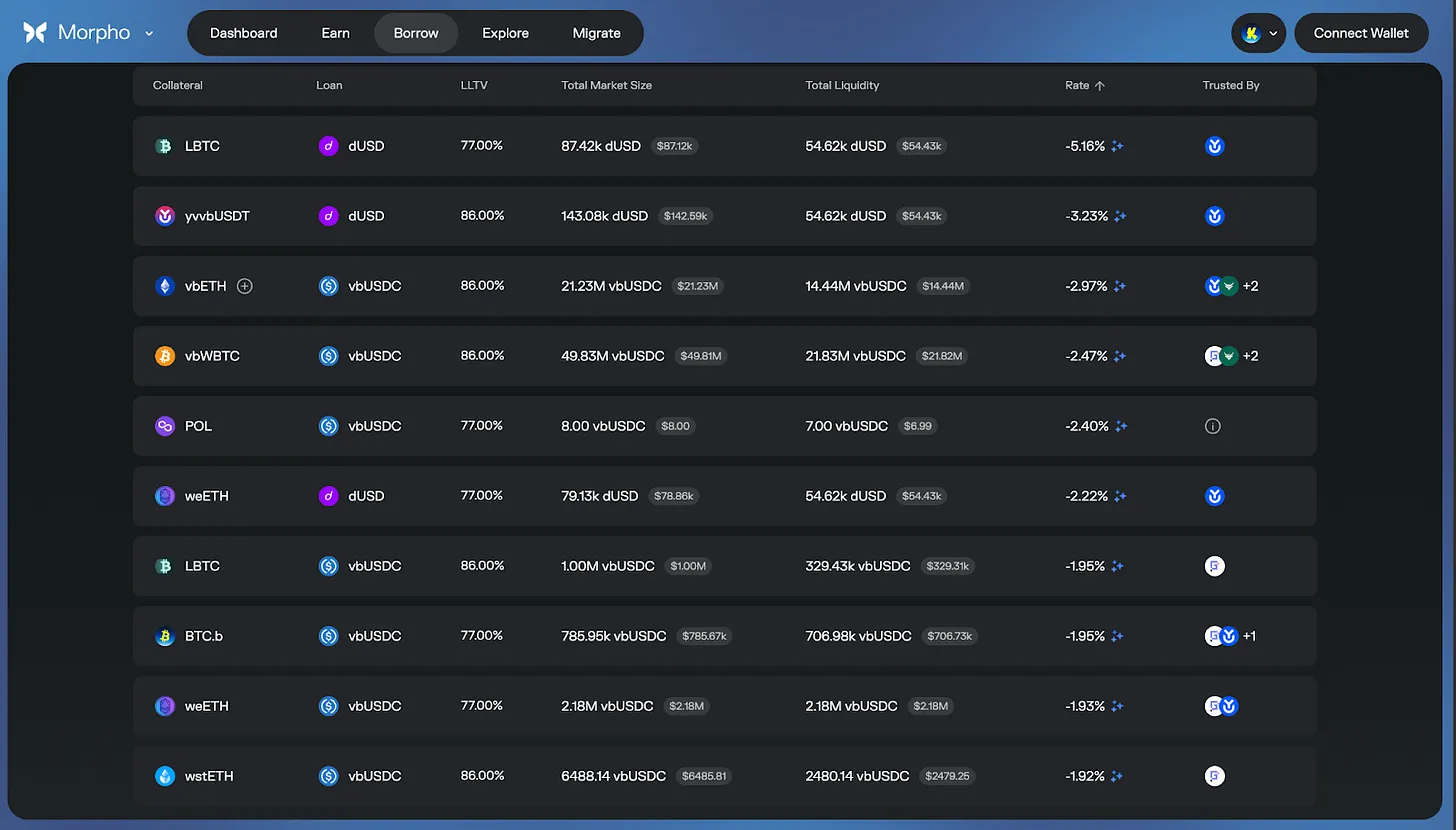

Katana’s incentive structure can significantly reduce actual borrowing costs at specific times, even creating negative interest rates depending on market conditions and reward schemes. This is because yields from Vault Bridge, CoL, and AUSD are reinvested into core markets. However, these are market-driven, incentive-based outcomes that fluctuate with conditions.

For this reason, by Q3 2025, over 95% of Katana’s TVL is actively deployed in DeFi protocols. In contrast, most chains’ capital utilization rates are only between 50% and 70%. Ultimately, Katana is building a capital chain that never sleeps—a system that truly rewards active use.

Katana never sleeps.