The earliest realistic scenario for Bitcoin to become the global reserve currency — in the sense of playing a dominant role within the reserve system rather than just being an additional reserve asset — could occur around the mid-2040s. This assessment is based on models viewing official regulations, collateral mechanisms, and pricing practices — international payments as decisive constraints.

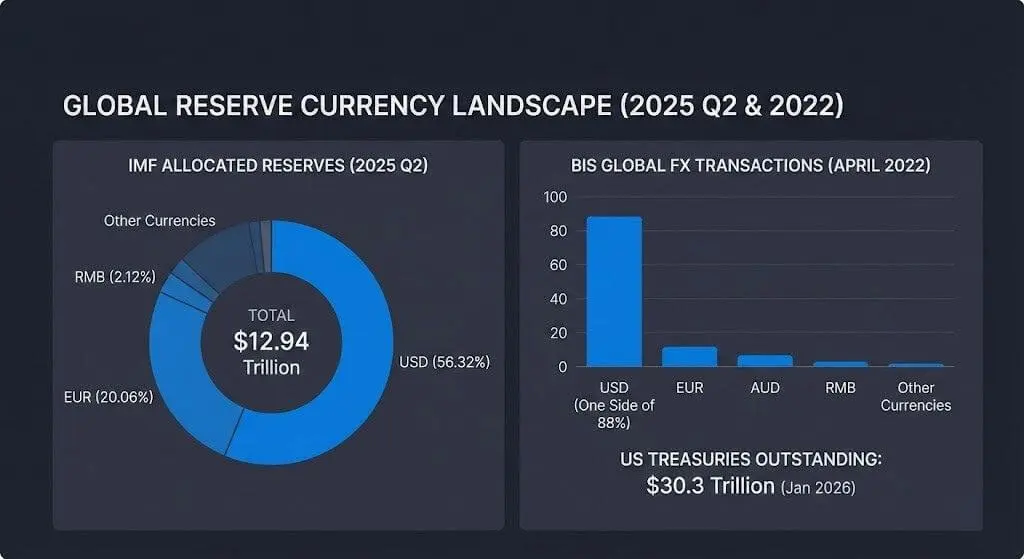

The starting point of the model is the current reserve system, where total global foreign exchange reserves reach $12.94 trillion in Q2/2025, with the US dollar still accounting for 56.32% of allocated reserves.

IMF data shows why it is very unlikely to expect a reversal within a decade, even if the private sector accelerates Bitcoin adoption. The size of the global reserve system is too large and changes very slowly.

In Q1/2025, IMF reports the USD’s share in global reserves at 57.74%, euro 20.06%, and yuan 2.12%. These figures reflect the “safe” balance sheet structure that central banks are operating under.

The reserve currency position is also closely tied to the supporting ecosystem behind the reserve portfolio. In April 2022, USD appeared on one side of 88% of global foreign exchange transactions.

The collateral assets of this network remain primarily US Treasury bonds. The total outstanding bonds are approximately $30.3 trillion, with an average daily trading volume of about $1,047.1 billion, according to US Treasury bond market statistics updated in January/2026.

Two steps: Reserve assets and dominant currency position

The story of Bitcoin becoming a reserve currency essentially involves two separate but often combined steps.

The first step is “reserve asset breakthrough,” where official institutions and regulated financial intermediaries regard BTC as a diversified long-term reserve asset with a limited share.

The second step is “dominant reserve currency position,” where BTC becomes the standard unit for trade valuation, payments, collateral, and cross-border liquidity provision.

The IMF’s “currency dominance” framework explains why pricing and contract practices can persist for a long time, even as trade structures change. Pricing and financing habits tend to reinforce themselves, both during normal periods and under market stress.

Meanwhile, policy and market infrastructure being developed can continue to enhance the role of USD rather than replace it. The Bank for International Settlements (BIS) reports that the Agorá project is researching the tokenization of wholesale central bank digital currencies and commercial bank deposits on programmable platforms for cross-border payments. This scenario shows that the currencies of major nations and bank balance sheets remain the “central monetary objects,” even as technological interfaces evolve.

In Citi’s 2025 stablecoin outlook report, issuance volume could reach $1.9 trillion by 2030 under the baseline scenario and $4.0 trillion under the optimistic scenario.

McKinsey also estimates that asset tokenization (excluding crypto and stablecoins) could reach around $2 trillion by 2030, with a range of $1–4 trillion. This indicates that financial balances could shift significantly toward digital formats without changing the accounting units of reserves.

Expanded access but official constraints remain

Access to Bitcoin within regulated frameworks has expanded, reducing one barrier to holding it as a reserve asset, but it has not yet addressed the challenge of becoming the dominant reserve currency.

On January 10, 2024, the SEC approved 11 Rule 19b-4 filings for spot Bitcoin ETPs, creating a standard investment structure for US investors and some institutions that cannot custody BTC directly.

Trading volume of crypto spot ETFs in the US has exceeded $2 trillion, and total assets of spot Bitcoin ETFs are around $117 billion as of January 2, 2026. However, this figure reflects market access channels more than governments’ reserve intentions.

In the short term, central bank behavior also shows another competitive diversification channel: gold. The World Gold Council reports that central banks bought about 1,045 tons of gold in 2024, marking the third consecutive year exceeding 1,000 tons.

A 2025 survey by the same organization indicates that 95% of central banks expect global gold reserves to increase, with a record 43% planning to increase their gold holdings over the next 12 months.

This actual capital flow limits models assuming that short-term official reserve diversification will automatically shift to BTC. Instead, Bitcoin must compete with an established reserve asset with long-standing accounting standards and liquidity.

Earliest milestone according to the model: around 2046

Projections for Bitcoin becoming the “global reserve currency” depend on a series of conditions that must be sequentially met:

- Price volatility decreases to levels compatible with reserve portfolios

- Legal and regulatory standardization of custody and settlement finality

- Funding and collateral markets are sufficiently deep to operate even during crises

- Official directives from the public sector go beyond symbolic allocations

- Changes in pricing, payment practices, or collateral use away from the current USD platform

The “moat” these conditions must overcome is clearly reflected in macroeconomic data: USD share in reserves, USD’s position in forex markets, and the scale of US Treasury collateral assets.

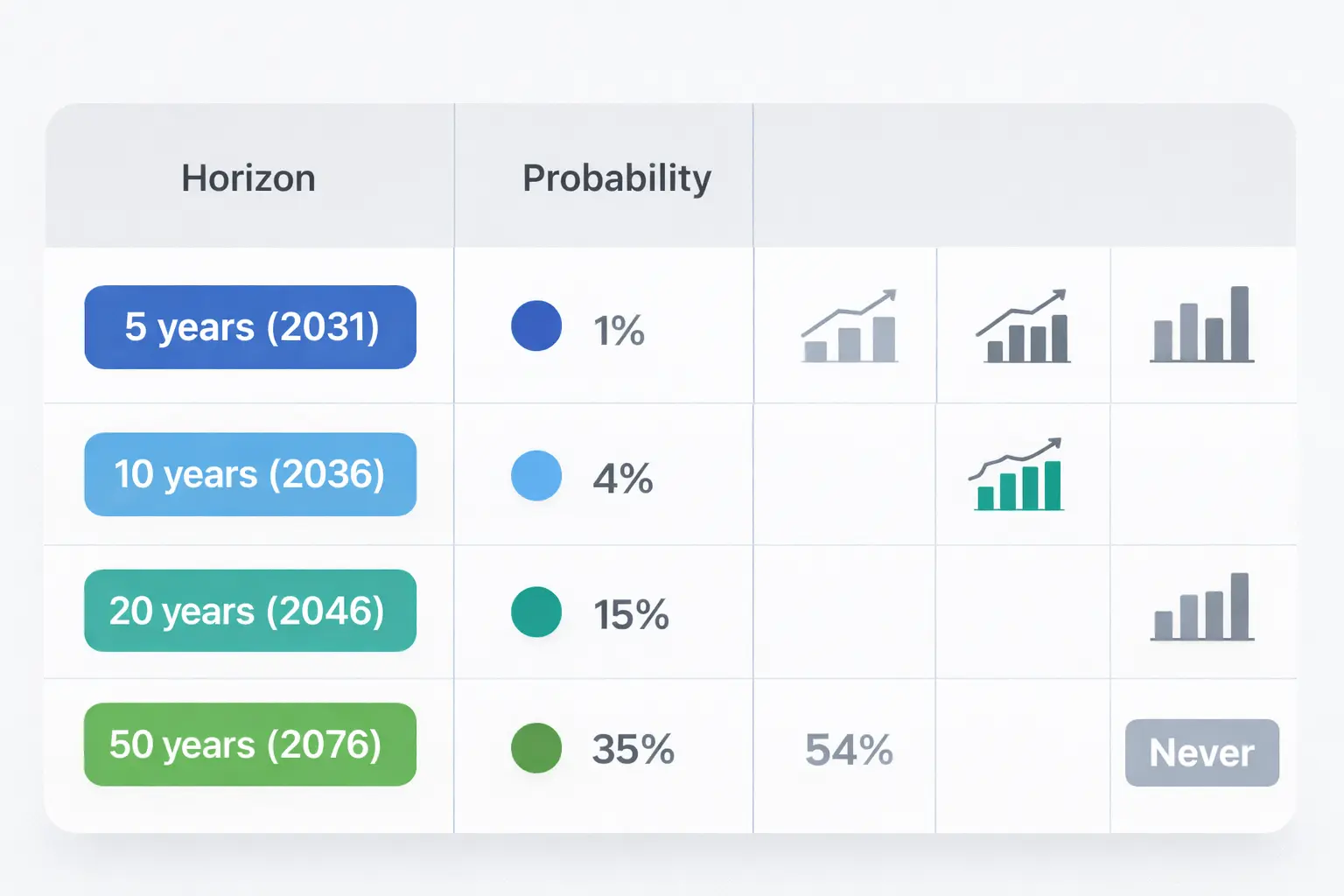

Based on these constraints, this scenario model suggests a “earliest window” for Bitcoin to achieve a dominant reserve currency status around 2046. This is separate from the possibility of BTC becoming a smaller-scale reserve asset in some portfolios earlier.

Probabilities at different time points (edited model)

| Time |

Probability of BTC becoming the global reserve currency |

Model assumptions linked to observable constraints |

| 5 years (2031) |

1% |

Existing ETP access channels, but reserve management requirements and official directives rarely change within a cycle, while USD reserve share and dominance in forex markets remain high (CRS; IMF COFER Q2/2025; BIS FX survey). |

| 10 years (2036) |

4% |

Tokenized deposits and USD-pegged stablecoins could expand on programmable infrastructure, reinforcing current currency use even as payment technology evolves (BIS Agorá project; Citi stablecoin framework). |

| 20 years (2046) |

15% |

Regulatory convergence over multiple cycles and the maturing of funding markets could create cumulative effects, though the foundation of US Treasury bonds and forex network effects remain significant (SIFMA Treasury market statistics; BIS FX survey). |

| 50 years (2076) |

35% |

Long time horizon allows for institutional restructuring, but the sustainability of the dominant currency in valuation and contract signing remains a structural obstacle (IMF’s currency dominance framework). |

| Never |

45% |

Structural barriers include the lack of issuing organizations supporting during crises and the potential for tokenized USD systems to absorb most digital currency needs (BIS Agorá project; Citi stablecoin framework). |

Conclusion

Aggregated data shows a clear separation between channels that can rapidly expand exposure to Bitcoin and those that change very slowly, determining reserve currency status.

Tokenized bank money and stablecoins could reach trillions of dollars within a decade but still keep USD and bank deposits at the core of payments. Central banks may continue increasing gold holdings as a hedge for their balance sheets while maintaining USD as the core foreign reserve.

These constraints make 2046 the “earliest window” for Bitcoin to reach a dominant reserve currency status in this model, rather than the median scenario. In the short term, the focus remains on whether Bitcoin can develop a sufficiently reliable liquidity infrastructure and collateral assets for reserve managers to hold through periods of stress.

Vương Tiễn

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.