Author: danny

Who would have thought that the modern cross-border tax information system was actually triggered by a “toothpaste”? A UBS banker smuggled diamonds by stuffing them into a tube of toothpaste, a Hollywood-style scene that unexpectedly sounded the death knell for Swiss banking secrecy laws. Today, the gears of history are relentlessly grinding toward the crypto world—once a secret “tax haven,” it is about to face its reckoning.

This article will unveil the mysterious veil of CARF: a global tax crackdown net. From Binance’s “capital relocation” to the UAE as a strategic game of trading space for time, to the harsh reality that “crypto-to-crypto” trades are no longer tax-exempt; from Hong Kong’s compliance countdown to mainland investors’ shattered illusions.

This is not only a reshaping of industry patterns but also a survival guide that every crypto asset holder must face—after all, in this algorithm-woven cage, no one can continue to bury their head in the sand like an ostrich.

Preface: What is CARF?

CARF stands for (Crypto-Asset Reporting Framework). Its core mechanism is that crypto-asset service providers (RCASPs) with reporting obligations collect client and transaction-related tax information, report it to the tax authorities of their jurisdiction, and ultimately, through automatic international intelligence exchange between tax agencies. Similar to the traditional CRS in finance, but CARF specifically focuses on buying, selling, exchanging, custody, and transfer of crypto assets.

Simply put, previously, users trading cryptocurrencies on exchanges made it difficult for their home tax authorities to fully grasp relevant information. Now, CARF links the user’s tax residence with the jurisdiction of the exchange. Once they establish a CARF cooperation, the user’s tax residence country can access detailed information about offshore crypto trading activities of its residents, enabling tax collection and enforcement.

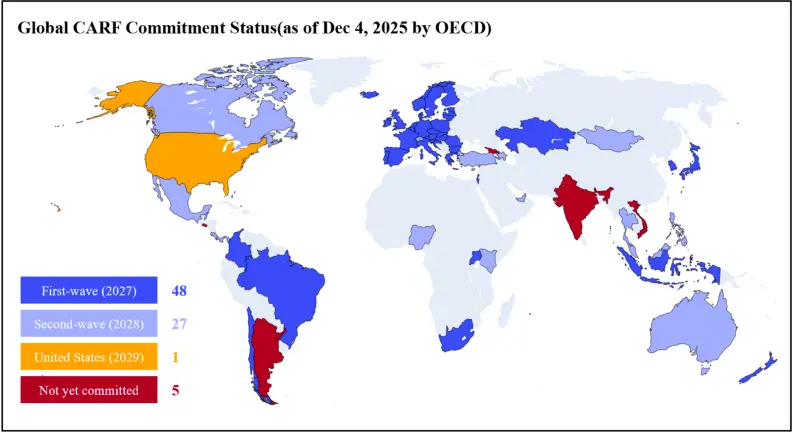

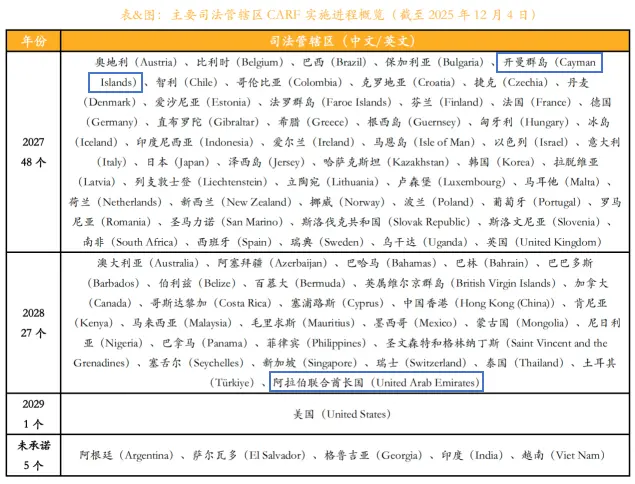

By the end of 2025, over 75 jurisdictions have committed to implementing CARF in 2027 or 2028, with more than half having signed relevant agreements with authorities. Starting from January 1, 2026, the CARF framework takes effect in the first 48 jurisdictions, covering the UK, EU, Japan, South Korea, Singapore, and others.

Chapter 1: Diamonds in the Toothpaste, the End of Secrecy, and the Arrival of CRS

To understand CARF’s “new sickle,” we must first look at the “old net”—CRS (Common Reporting Standard).

The protagonist is Bradley Birkenfeld, a former UBS client manager. He aimed to covertly bring back his client—American real estate tycoon Igor Olenicoff’s $200 million untaxed assets from UBS to the US.

Birkenfeld devised a Hollywood-worthy scheme: he bought diamonds, stuffed them into a tube of ordinary toothpaste, evaded customs X-ray scans, then confidently flew across the Atlantic, handing the diamonds to Olenicoff for liquidation.

In 2007, when Birkenfeld discovered in an internal bank report that he might become a scapegoat for internal compliance washouts, he made a rebellious decision: to turn against the Swiss banking industry’s traditions. He brought a batch of top-secret internal emails and client lists into the US Department of Justice.

Birkenfeld’s testimony directly led UBS to pay a record fine of $7.8 billion in 2009 and unprecedentedly handed over the names of over 4,000 US clients. This marked the death of Swiss banking secrecy laws. (Interestingly, Birkenfeld also received a bounty of $104 million in the end.)

The US Congress realized that relying solely on informants like Birkenfeld was insufficient; they needed an automated monitoring system. Thus, in 2010, the most aggressive tax law in history—the Foreign Account Tax Compliance Act (FATCA)—was born. Its logic was simple and brutal: “Any bank worldwide that wants to do business with the US must report the account balances of US persons annually.”

Seeing FATCA’s immediate effect, OECD began to replicate it one-to-one. In 2014, the global standard based on FATCA—the CRS (Common Reporting Standard)—was officially launched.

This is why CRS’s underlying logic is very similar to bank transaction monitoring: it assumes wealth ultimately accumulates in bank accounts, generating interest and balances. It is a monitoring system tailored for the “fiat era,” aiming to make hidden wealthy individuals transparent through annual “balance snapshots.”

Just as everything was progressing toward regulatory expectations, a new entity—Bitcoin—was quietly growing. This “balance monitoring” CRS system is about to face an unprecedented opponent it never envisioned.

Chapter 2: The Hole in the Old Net—Why Do We Need CARF When CRS Exists?

Using an AI analogy, CARF is like a 24/7 high-definition camera installed at every compliant exchange’s entrance.

The biggest difference from CRS is: CRS checks “how much money you have,” while CARF checks “where your money flows.”

2.1 Origin and Strategic Intent of CARF

CARF was born out of G20 countries’ fear of tax base erosion. While CRS has been effective against offshore tax evasion, it mainly targets traditional bank and custodial accounts. Crypto assets, due to their decentralized, peer-to-peer transfer capabilities without intermediaries, became a blind spot for CRS.

OECD explicitly states that CARF aims to eliminate this blind spot by including crypto-asset service providers (CASPs) under the same information reporting obligations as banks. By the end of 2025, over 50 jurisdictions—including the UK, Canada, France, Germany, Japan, Cayman Islands, and others—have committed to implementing CARF. Data collection in these jurisdictions began quietly on January 1, 2026, with the first information exchange scheduled for 2027.

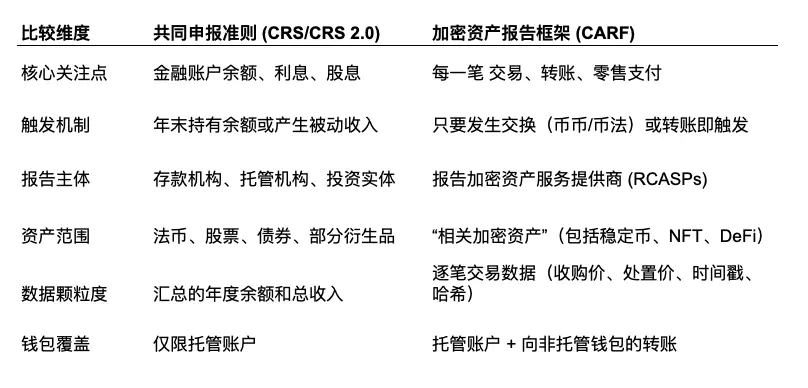

2.2 Comparing CARF and CRS 2.0: From “Stock” to “Flow”

CRS’s core logic is monitoring “stock wealth,” while CARF’s core is tracking the flow of wealth.

Under CRS, besides year-end balances, tax authorities see almost no intermediate process. Under CARF, every action—such as converting Bitcoin to USDT, transferring USDT to a cold wallet, or purchasing over $50,000 worth of $PUNDIAI (retail payment transactions)—generates a report record. CARF effectively elevates the view from a “static balance sheet” to a “dynamic cash flow statement.”

2.3 Scope of “Related Crypto Assets”

CARF’s definition of “related crypto assets” covers most types of crypto assets:

Stablecoins: Although many claim to be fiat substitutes, under CARF, they are explicitly regarded as crypto assets. This means that exchanging USDT for USD may no longer be a “currency exchange” but a taxable transaction.

NFTs: While CARF mainly focuses on assets used for payment or investment, high-value NFTs with secondary market trading attributes are likely to be included in reporting.

Tokenized securities: Even tokenized stocks or bonds already regulated in traditional financial markets, if on-chain, may be subject to both CRS and CARF (despite OECD’s attempts to revise CRS to avoid duplication, in practice, overlapping reporting is hard to avoid due to the “better to kill wrong than miss” principle).

Chapter 3: Retail Investors’ Pretensions, Illusions, and Disillusionment

3.1 Crypto-to-Crypto Trading: Mandatory “Fair Pricing” Mechanism

CARF requires that all crypto-to-crypto exchanges record the fair market value in fiat currency at the moment of the trade.

In the eyes of tax authorities, crypto-to-crypto trades are equivalent to “selling first, buying later.” Many people mistakenly believe: “If I exchange Bitcoin for Ethereum without converting to fiat, I don’t sell, so no tax.” That’s a delusion for the naive.

CARF mandates exchanges to record: “On a certain date, Zhang San exchanged 1 Bitcoin for 20 Ethereum, and at that time, 1 Bitcoin was worth $50,000.” In the eyes of tax authorities, this is a taxable event of “selling Bitcoin for $50,000.” Even if you hold no cash, your tax record is already generated.

CARF will thoroughly end the tax avoidance strategy of “funding coins with coins.” After 2026 (or 2027 in some regions), every crypto swap will be recorded as an asset disposal event, leaving a definite “fiat profit record” in your tax file—regardless of whether you cash out into fiat or stablecoins.

3.2 Wallet Penetration: Transaction Hashes and Address Cleaning

In CARF’s XML schema, RCASP is required to report specific transaction types and values. Although, after strong industry lobbying, the mandatory reporting of all non-custodial wallet recipient addresses was removed, internal systems still collect and retain this address and its associated beneficiary information for at least 5 years (“retention rule”).

This means tax authorities have the right to access data at any time. If they find a taxpayer has large “withdrawal” records in 2026 but no subsequent declared income, they can issue bulk information requests to exchanges, precisely obtaining external wallet addresses.

When you withdraw coins from an exchange to your personal wallet or cold storage, the exchange must record and report (“if requested”) “which address was involved.” It’s like withdrawing cash from a bank: the bank not only records how much you withdrew but also tracks who you are and which safe deposit box you used. Once your wallet address is linked to your real identity in the tax database, all your on-chain DeFi activities are essentially “naked.”

3.3 Standardized Valuation Anchors

If trading two obscure tokens (e.g., exchanging “air coins A” for “air coins B”), what if there’s no fiat trading pair? CARF prescribes a “cascading valuation method”: if asset A has no fiat price, reference asset B’s fiat price; if neither has, service providers must use a reasonable valuation method to set a price. In any case, a fiat value must be generated and sent to the tax authorities. This eliminates the loophole of fuzzy valuation based on price fluctuations during tax reporting.

3.4 Mandatory Taxpayer Identification Number (TIN)

CARF requires RCASP to collect users’ tax residency and corresponding TIN. However, if a user only declares a low-tax jurisdiction (e.g., Dubai), but the exchange finds through IP, phone area code, or login logs that they frequently operate in higher-tax jurisdictions (e.g., France), the exchange is obliged to question the reasonableness of this self-certification.

Chapter 4: The Trap of Retroactivity—2026 as the “Year of Exposure”

Many old-timers believe that as long as assets are handled before the first information exchange in 2027, everything is fine. That’s incorrect. They overlook CARF’s “retrospective effect,” meaning that the 2027 data exchange involves reporting for 2026.

4.1 “Opening Balances” and Historical Audits

When tax authorities receive CARF data for 2026 in 2027, they will first focus on “opening balances” or “annual transaction totals.”

Scenario simulation:

Suppose Mr. Zhongben, a Chinese investor, sold $10 million worth of $PUNDIAI tokens through a compliant Hong Kong platform in 2026. The platform reports this data to the tax authorities under CARF. The tax AI system will immediately compare this with Mr. Zhongben’s previous tax declarations. If he never declared overseas crypto holdings before, the source of this $10 million will become a huge suspicion.

The tax authority can trace back the hash of this transaction to find out when these $PUNDIAI tokens were bought. If purchased in 2024, then all unrealized gains from 2024 to 2026 will be exposed.

Note that many countries’ tax agencies have deployed AI-based big data analysis systems specifically for identifying mismatches between asset holdings and declared income. We expect 2026 to be a “tax collection storm” for crypto billionaires.

4.2 The Compliance Window of 2026

For non-compliant investors, 2026 is essentially the last window. Before the data gate closes, investors face tough choices:

- Voluntarily declare past assets, possibly reducing penalties.

- Reorganize holdings under compliant structures (e.g., family trusts, offshore companies) or seek professional tax advice to plan crypto assets reasonably. (Advertising space is open for bidding~)

Chapter 5: Binance’s Relocation: Trading Space for Time

Why did Binance choose Abu Dhabi among many regulator-friendly jurisdictions? Besides local policy support and capital channels, an important factor is the compliance time gap.

Binance’s original base was the Cayman Islands, one of the first jurisdictions to implement CARF, with the first data exchange scheduled for 2027. This means RCASPs must start collecting and storing data for reporting from 2026. If Binance stays in Cayman, it must immediately build a comprehensive CARF compliance system.

In contrast, the UAE is in the second batch of jurisdictions implementing CARF, with data exchange planned for 2028.

From Cayman to UAE, Binance gains a strategic buffer of one year. For a platform serving over 300 million users, this period is crucial:

First, avoid early risks. Observe how the first batch jurisdictions operate, learn from other exchanges’ experiences, and optimize compliance plans.

Second, participate in rule-making. Currently, UAE’s CARF legislation and implementation details are still being drafted. As a major exchange, Binance can influence the process, voice opinions, and negotiate with authorities to shape favorable local rules.

Third, complete system upgrades. This year provides ample time for Binance to deploy and test a data reporting and management system that meets CARF’s complex requirements.

This is the so-called “trading space for time.”

Chapter 6: CARF in China: Impact and Trends

As one of the largest global crypto user markets, China’s situation is unique.

Some say mainland China is not among the first signatories of OECD’s CARF, so trading crypto in Hong Kong is invisible to mainland tax authorities—this is a misconception.

China has not joined or committed to implementing CARF, so mainland tax authorities do not access Chinese residents’ crypto transaction data via CARF. But this doesn’t mean Chinese crypto billionaires can relax. China is already an active participant in CRS. Although CARF targets crypto assets, if they are exchanged for fiat and deposited into banks, or held as financial assets (like ETFs), they are already within CRS’s monitoring network. Additionally, consultation documents mention that CARF information will be exchanged with “partner jurisdictions.”

Attentive readers will notice that Hong Kong is in the second tier of CARF implementation, with ongoing legislative consultations on CARF and CRS amendments, and a clear roadmap to complete legislation by 2027, with information exchange starting in 2028.

Under the “dual-track” crypto regulation framework, the impact of CARF in China should be viewed separately:

Hong Kong-based crypto users have the obligation under CARF to submit self-certification data to exchanges. Subsequently, their offshore crypto trading data will be exchanged with Hong Kong tax authorities via automatic mechanisms. This increases transparency, making it harder for users to evade taxes through decentralization or anonymity.

Meanwhile, Hong Kong exchanges acting as RCASPs must strengthen KYC, build data collection and reporting systems. Failure to register, report, conduct due diligence, or submit inaccurate information may trigger legal liabilities, with fines up to millions HKD.

In contrast, mainland China’s short-term impact from CARF is limited, partly due to its stance on crypto assets as “illegal.” But the trend toward tax transparency is unstoppable, and mainland Chinese residents will find it increasingly difficult to remain “unaffected.” As Hong Kong joins the global information exchange network under CARF, China may also access crypto transaction data from Hong Kong or join CARF in the future.

For mainland investors, the era of relying on Hong Kong as a “safe haven” is over. Although automatic exchanges may have a lag of several years, “on-demand exchange” channels remain open, and data retention rules ensure that historical records can be accessed at any time.

Chapter 7: Survival Guide—Don’t Be an Ostrich with Your Head in the Sand

If you ask a Korean oppa, he’ll tell you there are three unavoidable things in this world: life and death, Samsung, and taxes.

As individuals caught in this tide of change, what should we do?

Pay attention to the tax consequences of “crypto-to-crypto” trades: Don’t be naive to think that not withdrawing means no taxes. From now on, every “buy/sell” click might trigger tax obligations. (In countries with capital gains tax)

Organize your accounts: Clear out “zombie accounts” on unknown small exchanges or those registered with fake identities. Either close them or withdraw your coins. When CARF’s net falls, these accounts will be among the first to be scrutinized.

Understand cold wallets: They remain your last data fortress, but the bridges in and out are now monitored. Transferring from Binance to a cold wallet is itself a record. Tax authorities may not see everything inside your cold wallet, but they know: “This address belongs to Zhongben Village, and he transferred 10 Bitcoin there in 2027.”

Follow the UAE and Hong Kong schedules: Both are in the second batch (2028 exchange). You still have about one or two years to adapt and plan. Use this time to learn compliance or seek professional tax advice—much more practical than searching for the next “tax haven.”

Postscript

Thanks to @FinTax_Official for professional analysis of tax laws and jurisdictional insights, which enriched the practical perspective of this article.